Canadian Office Trends Suggest Some Difficulties in 2024

Canadian Office Trends Suggest Some Difficulties in 2024

Like its southern neighbour, Canada’s office sector is confronted with several trends that are likely to shape occupancy patterns in 2024 and beyond.

These trends include the staying power of hybrid workplace strategies and weakening office sector employment growth, which are both combining to weigh on leasing fundamentals already. In addition, Canada’s office buildings under construction as a percent of existing inventory is at 2.8% — over double that of the U.S. at 1.3% — and much of this construction is concentrated in downtown centres that were hit hard from hybrid work.

This new supply risks further aggravating leasing fundamentals in the near term, especially in the context of a slowing economy.

The first trend facing Canada’s office sector, like in the U.S., is the staying power of hybrid workplace strategies. Many companies had adopted these policies that allowed office workers to telecommute during the pandemic. Yet six months after the World Health Organization declared an end to the pandemic health emergency, many employees are still working remotely several days a week. In fact, the latest office occupancy and mobility data for downtown Toronto shows that the new hybrid workplace is here to stay for many office workers, who likely prefer commuting less.

Even for the overall Toronto Census Metropolitan Area, or CMA, mobility remains well below where it was pre-pandemic. This indicates that suburban office submarkets, which often employ more people locally, have also been affected by the growth in hybrid workplace trends, although less so than their downtown counterparts. Although the below data is for Toronto, Canada’s largest office market, similar trends exist in other Canadian cities.

The second structural trend affecting the country’s office market is the slowdown in office employment growth. Office employment growth in Canada averaged 2.35% per year between 2001 and 2022. Excluding the volatility around 2020 through 2022, in which employment growth cratered and then rocketed to recovery, the country’s most robust office employment growth appeared between 2001 and 2008. During this period, Canada’s office employment growth regularly exceeded the long-term average of 2.35%.

In the years following the Great Recession, office employment growth tended to be spotty, with a brief outperformance occurring between 2017 and 2019. Moreover, Oxford Economics forecasts that office employment growth will decelerate over the coming decade.

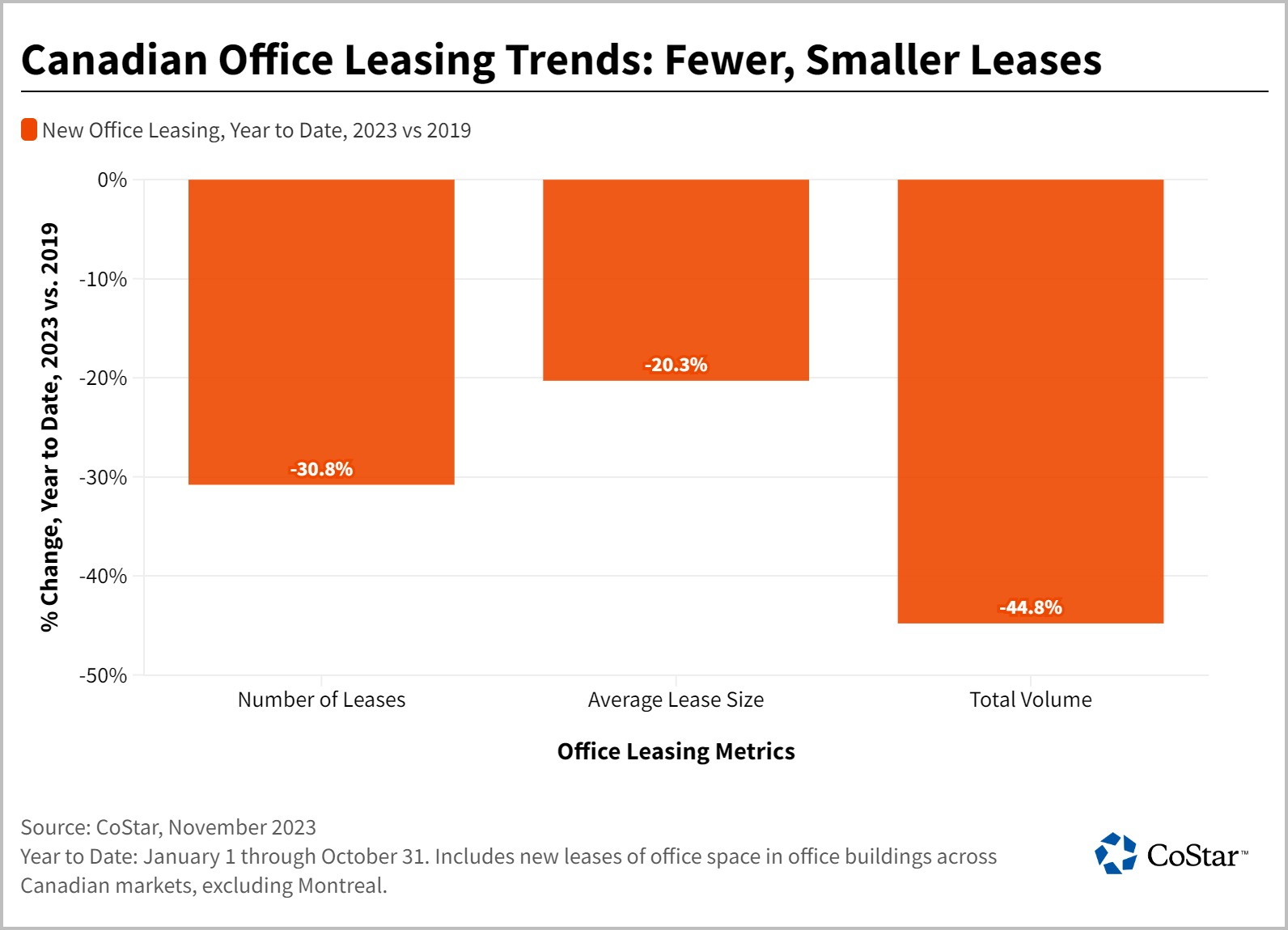

These twin trends of greater workplace flexibility and a downshift in office employment growth already appear to be taking a toll on the country’s office leasing sector. Occupiers are signing fewer new office leases and taking less space when they do sign. In fact, nearly a third fewer new office leases deals were signed in the first 10 months of 2023 compared to the first 10 months of 2019.

When occupiers are signing new leases, it is for 20% less space. This combination of fewer leases being signed coupled with smaller lease sizes translates into a total leasing volume that is nearly 45% below pre-pandemic levels.

At the same time, Canada’s office sector is building more stock relative to its inventory than the U.S. Although in pre-pandemic times, this construction pipeline was seen to help restore some balance in Canada’s office market given tight conditions, in the context of hybrid work and structurally lower office unemployment growth, the delivery of new space is likely to add to current leasing headwinds. This is especially so for older office stock, which will be competing with new buildings, as certain occupiers will likely be inclined to take space in newly delivered Class A product as opposed to staying in their existing older space.

The structural rise of hybrid work, coupled with a decline in office employment, are weighing on Canadian office leasing fundamentals. New office deliveries over the coming quarters will further weigh on leasing fundamentals, especially for older office stock. Overlaid across all these trends is a weakening economic outlook for the country, which is likely to slow the office sector’s recovery even further as businesses increasingly cut back on investment and trim expansion plans. Taken together, these trends suggest that next year is likely to be a another difficult one for Canada’s office sector.

Source CoStar Click here to read a full story

Comments

Leave a Reply

Leave a Reply

FOR LEASE – Office Spaces – Scarborough

Available units: #218 – 1,248 SF – $11.00 psf + $19.01 TMI psf #221 – 777 SF ̵ ...

FOR LEASE – Retail Space – Toronto

Available area: 595 SF Lease rate: $1,800.00 Net Lease Located in Toronto’s upscale Leaside ne ...

BUSINESS FOR SALE – Sports Equipment Shop – Peterborough

Available area: 783 Sq Ft Asking Price: $300,000.00 An exclusive business opportunity awaits in Pete ...

FOR LEASE – Office Space – Toronto

Available area: 1,124 SF Lease rate: $17.00 Net Lease Perfectly located near the 401 with easy trans ...

FOR LEASE – Office Space – Toronto

Available area: 755 SF Lease rate: $1,800 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Scar ...

FOR LEASE – Office Space – Toronto

Available area: 638 SF Lease rate: $1,700 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Sc ...

FOR LEASE – Office Space – Toronto

Lease price: $23.50 Sq Ft Net + $17.68/2023/T.M.I. Available area: 3,901 Sq Ft 1,820 Sq Ft Elevate y ...

FOR SALE – Development Site – Woodstock

Size: 1.14 acres Currently has a commercial building whihc is built out for Resteraunt/Banquethall/ ...

![]()

Toronto Commercial Properties

Stephen & Mariya Lilly

Brokers

Office: 416-494-7653

Mariya Cell: 416-824-5078

Stephen Cell: 416-802-4228

Puravive | Jan 25,2024

I loved even more than you will get done right here. The overall look is nice, and the writing is stylish, but there’s something off about the way you write that makes me think that you should be careful what you say next. I will definitely be back again and again if you protect this hike.