It’s Slowing Down The Demand For B- and C-Class Product and Increasing The Demand For A- and AAA-Class Product

It’s Slowing Down The Demand For B- and C-Class Product and Increasing The Demand For A- and AAA-Class Product

Canadian class-AAA office product is doing well, industrial remains hot and retail has rebounded, according to JLL Canada chief executive officer Alan MacKenzie and a new national outlook report.

The national office vacancy rate rose 40 basis points to 14.7 per cent in the second quarter, but MacKenzie told RENX that’s comparatively low from a global perspective.

Vancouver’s office vacancy rate of 7.3 per cent is the lowest in North America while Calgary’s 26.8 per cent rate is the highest. However, Alberta’s largest city is showing signs of a bounce-back due to a rebound in the oil and gas industries that has resulted in some companies taking sublet space off the market.

JLL expects the office vacancy rate to continue to rise across Canada, given the current economic uncertainty, which will bring balance to markets that have favoured building owners for several years.

Return to office has spinoff benefits

Several major institutional office occupiers have started mandating employees back to the office two to three days a week.

“As occupiers bring their people back for more days of the week in the downtown areas of Canada, we’re predicting a really positive impact on the surrounding retail, with people buying coffees and lunches and socializing after work with cocktails and dinners,” said MacKenzie.

Office occupiers are also trying to determine how much space they’ll need over the next 10 to 15 years and how to design it to attract and retain employees and enhance productivity.

Environmental, social and governance, air and light quality, design and accessibility are all top of mind as the flight to quality by office occupiers which picked up in earlier waves of the pandemic has continued.

High demand for class-A and -AAA office space

“It’s slowing down the demand for B- and C-class product and increasing the demand for A- and AAA-class product,” said MacKenzie.

Owners of class-C office space on the periphery of downtown Calgary need to be more aggressive with inducements and pricing to attract tenants, while owners of AAA space in downtown Toronto don’t have to offer incentives because there’s ample demand and scarce availability, MacKenzie added.

There’s an increasingly high demand for built-out space, as tenants don’t want to spend the time or money to improve their real estate unless it’s absolutely necessary.

The flight to the suburbs that occurred with some office occupiers during earlier stages of the pandemic is being reversed and many are looking to return downtown, according to MacKenzie.

Net rental rates fell from a historically high $20.52 per square foot in the first quarter to $20.22. Montreal was the only major market with an increase as office rents rose by 5.4 per cent.

Industrial vacancy very low

After five consecutive quarters of declines, the national industrial vacancy rate remained steady at 1.5 per cent in Q2. Vancouver’s vacancy rate was 0.8 per cent, Toronto’s was 0.9 per cent and Montreal’s was 1.7 per cent, while Calgary’s rate dropped by 290 basis points year-over-year to 1.7 per cent.

“Because of the length of time it takes to entitle land and develop industrial product, and the limitation of available land, we can’t build it fast enough in order to meet the demand,” said MacKenzie.

“Notwithstanding that there are some headwinds with the economy and interest rates and the potential for a recession to be coming up that could put a little pressure on the demand side from occupiers, the scarcity of product is so rampant that we don’t see it as a risky place at this stage of the game.

“It’s still a very healthy market and it’s healthy to be an investor in that space right now.”

Industrial vacancies are expected to rise modestly but will remain landlord-favourable over the next few years, the report states.

Industrial rents continued to rise at an exponential rate across the country. Average asking net rents hit $12.11, a 17 per cent increase year-over-year, after expanding 14.4 per cent in Q1. While Canada’s three largest markets continued to expand 20 per cent and more year-over-year, Calgary and Winnipeg entered double-digit territory with rents increasing 11.6 and 10.4 per cent, respectively.

Southwestern Ontario had a surprisingly large and unanticipated 41.2 per cent year-over-year industrial rent increase.

“Land is less expensive in Southwestern Ontario so the overall production costs of building there are less than it would be in the Greater Toronto Area and developers are able to pass along those cost savings with slightly lower rental rates than the GTA,” said MacKenzie.

“We’re also seeing more and more Toronto-based investors and developers buying land in Southwestern Ontario and developing industrial product to try and take advantage of that demand and opportunity.”

MacKenzie expects rents to continue to increase for the next couple of years as supply trails demand.

Industrial transactions reached $4.1 billion in Q2 – a 58 per cent increase over the five-year quarterly average – though not quite as high as the all-time high of $5.3 billion in Q1. Pricing was at an all-time high with an average of over $242 per square foot.

More than 11 million square feet of industrial projects were started in the second quarter. Total space under construction was almost 48.4 million square feet, a five-million-plus-square-foot increase quarter-over-quarter.

Retail has rebounded

Canada had harsher and longer COVID-19 lockdowns than many other countries, which created wealth as people saved more money since there were fewer places to spend it.

Now that lockdowns are over, people are spending money on restaurants, entertainment and experiential retail, as well as clothing and shoes as more workers return to offices.

Accelerating wage growth and record lows in unemployment suggest people will keep spending, but high inflation and rising interest rates may curb discretionary purchases.

In-store purchases continue to trend up while e-commerce has trended down in the short term. The long-term outlook remains positive for e-commerce, however, because shoppers still like the convenience.

“Notwithstanding the disruption in retail as an industry during COVID, there has been a resurgence of investor demand in purchasing retail — specifically grocery-anchored retail in strong trade areas,” said MacKenzie, who noted pricing for class-A grocery-anchored retail in strong trade areas is higher than before the pandemic and the number of bids for it is high.

Transaction activity has been strong

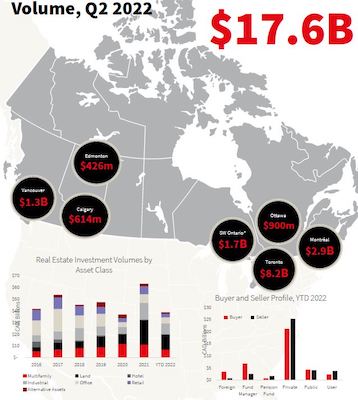

There was $17.6 billion in multiresidential, industrial, land, office, hotel, retail and alternative asset class investment transaction volume in seven large Canadian markets during Q2, the JLL report states.

Toronto led the way with $8.2 billion, followed by Montreal with $2.9 billion, Southwestern Ontario (Hamilton, Kitchener, Waterloo, Cambridge, Guelph, Stratford, Woodstock and Brantford) with $1.7 billion, Vancouver with $1.3 billion, Ottawa with $900 million, Calgary with $614 million and Edmonton with $426 million.

Transaction activity was very strong in the first half of the year and private buyers and sellers were the dominant players.

Institutional investors have focused on the asset management of existing portfolios, trying to mitigate risks and drive value through leasing, redevelopment and capital expenditures over the past two years.

“They’re all internally looking at their portfolio allocations very carefully and how much exposure they have in office, retail, multifamily and industrial, and the exposure geographically, in order to set strategies for the future and take advantage of future trends of growth,” said MacKenzie.

“They’ve become portfolio analysts of their own portfolios much more heavily than they were five years ago.”

Shrinking buyer pool for some office product

There’s a shrinking pool of buyers for class-B and -C office product and even for class-A product in weaker markets such as Calgary and Edmonton, MacKenzie said.

“Now we’re going through a period of price discovery for some of the asset classes and markets because interest rates have gone up and the cost of carrying debt has put downward pressure on the ability of some buyers to have appropriate spreads over their debt costs.”

Vancouver, Toronto and Montreal class-AAA office product is in high demand and MacKenzie said there’s ample institutional and private capital waiting for trophy assets to become available.

Ivanhoe Cambridge outsourced property management and leasing for its 16-million-square-foot shopping centre portfolio to JLL last October and other investment management companies and institutional investors are evaluating that model.

“Maybe there’s an opportunity to move faster and become more efficient at growing their assets under management if they outsource the property management and leasing functions of their business,” said MacKenzie. “We anticipate this outsourcing trend to accelerate, not just in Canada but globally over the next several years.

“They’ll focus on their investment management activities in trying to grow their assets under management.”

Source Real Estate News EXchange. Click here to read a full story

Leave a Reply

Leave a Reply

FOR LEASE – Retail Space – Toronto

Available area: 595 SF Lease rate: $1,800.00 Net Lease Located in Toronto’s upscale Leaside ne ...

BUSINESS FOR SALE – Sports Equipment Shop – Peterborough

Available area: 783 Sq Ft Asking Price: $300,000.00 An exclusive business opportunity awaits in Pete ...

FOR LEASE – Office Space – Toronto

Available area: 1,124 SF Lease rate: $17.00 Net Lease Perfectly located near the 401 with easy trans ...

FOR LEASE – Office Space – Toronto

Available area: 755 SF Lease rate: $1,800 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Scar ...

FOR LEASE – Office Space – Toronto

Available area: 638 SF Lease rate: $1,700 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Sc ...

FOR LEASE – Office Space – Toronto

Lease price: $23.50 Sq Ft Net + $17.68/2023/T.M.I. Available area: 3,901 Sq Ft 1,820 Sq Ft Elevate y ...

FOR SALE – Development Site – Woodstock

Size: 0.9 acres The two building lots are designed to be mixed-use, with commercial spaces on the gr ...

FOR SALE – Development Site – Woodstock

Size: 1.14 acres Currently has a commercial building whihc is built out for Resteraunt/Banquethall/ ...

![]()

Toronto Commercial Properties

Stephen & Mariya Lilly

Brokers

Office: 416-494-7653

Mariya Cell: 416-824-5078

Stephen Cell: 416-802-4228