Author The Lilly Commercial Team

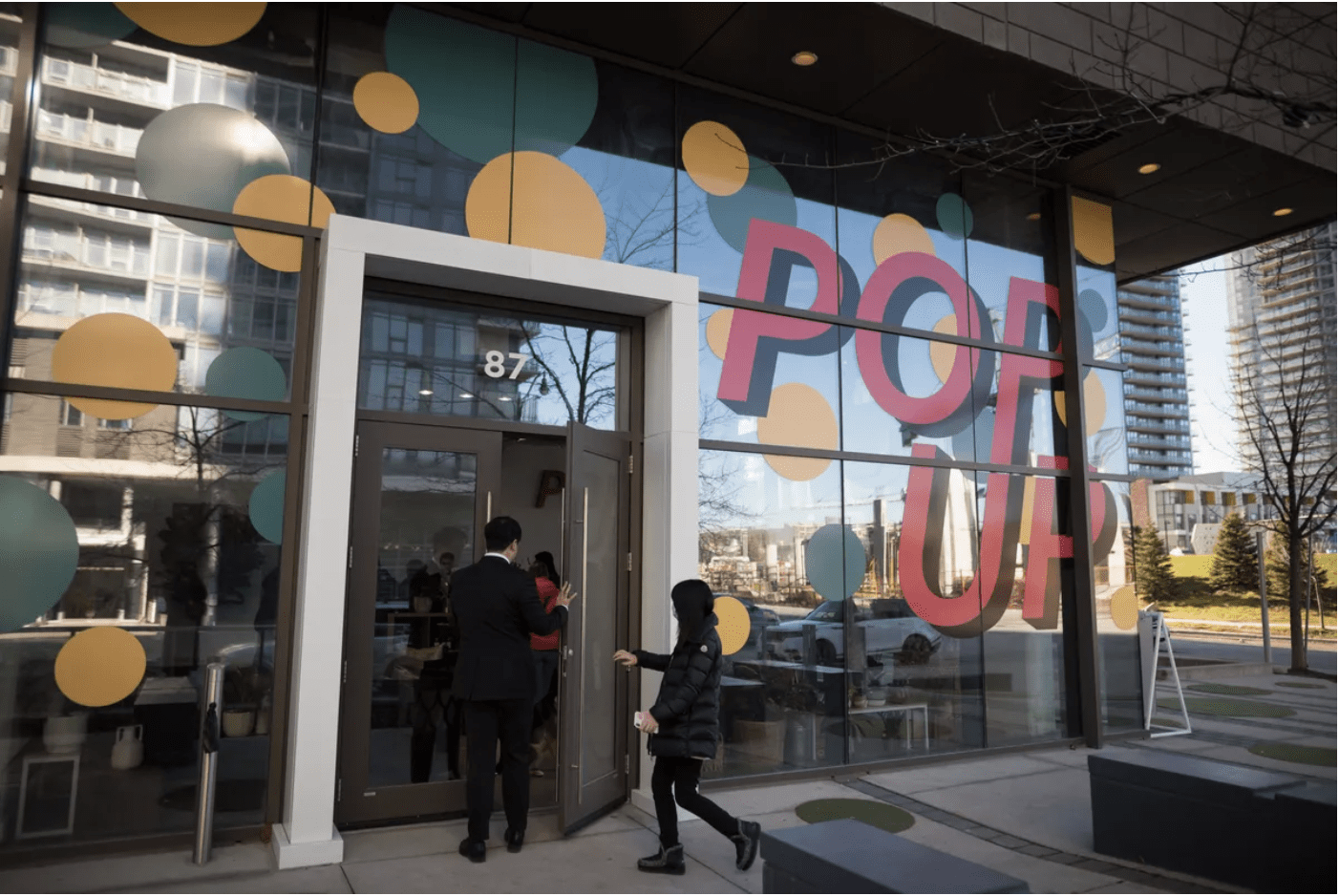

Filling In The Retail Spaces In The Second Largest Master-Planned Development in Toronto is a Problem, or an Opportunity, Depending on How You Look At It.

On a given day most people who come to the Concord Park Place real estate development in Toronto are there for some do-it-yourself furniture or meatballs from the IKEA it shares space with.

Concord’s site is sandwiched between Highway 401, a six-lane stretch of Sheppard Avenue and tracts of single-family homes: it is the definition of a car-centric community.

This is true in spite of the nearby Bessarion subway station (long in the Hall of Shame as Toronto’s least-used subway stop) and despite the fact that Concord is going to add almost 5,000 apartments to the 45-acre site (formerly a Canadian Tire distribution centre) and pepper the landscape with as many as 20 towers by the time all is said and done. This level of density is practically unheard of in North York, and it presents an opportunity to create a walkable streetscape in a part of Toronto not known for having many. This is strip mall and Big Box retail country (as the nearby Canadian Tire and IKEA would attest).

That’s why Isaac Chan, vice-president of sales and marketing at Concord Adex, an arm of the B.C.-based Concord Group, has spent much of 2022 experimenting to create a walkable high street by temporarily hosting a variety of retailers, cafés and community installations in a pop-up store location in one of its Park Place buildings across from recently finished Ethennonnhawahstihnen’ Park.

“We’ve had about eight in here,” said Mr. Chan, standing inside the most recent pop-up, a flower-shop/café called Olivia’s Garden. “Some of them said, ‘We just want to try for a weekend’ and then expanded to more weeks so that they can kind of feel out the community.”

Concord marketing specialist Tanya Kolacz found Olivia’s Garden on Instagram, and was drawn to the elegance of the offering: specialty pottery, minimalist design, coffees infused with edible flowers and unique floral arrangements while you wait.

The café opened during the pandemic in its sole location on Harbord Street in downtown Toronto, a tumultuous business environment that café manager Jason Korol says allowed the company to experiment with its unique caffeinated offerings.

“For example, we have a blue lavender drink and we grow the lavender [for the syrup],” he said, which is also harvested in spring, summer and fall to distill syrups from different stages of the plant’s life. “Depending on the season you come in it’s a slightly different flavor. So it’s the same song, but kind of like a different melody.”

One of the first pop-ups Concord hosted in July also married plants and coffee: connecting specialty roaster Terminal 3 (which plans to return to the pop-up soon) with plant retailer JOMO, which is an existing retail tenant in its City Place development. Over the summer and fall the pop-up site has hosted the Boxcar Social café, Courage Cookies, Hielito Bites (a purveyor of Mexican desserts) as well as art gallery installations and a physical pop-up of online function fashion retailer Stage 9 Secrets.

One thing many of these shops have in common is their permanent locations tend to be in walkable downtown neighbourhoods that grew up in a sometimes chaotic fashion over decades. A frequently referenced element of urbanist Jane Jacobs’s writing is the idea of the “sidewalk ballet” that makes up a lively streetscape: a mix of residents and visitors blending together throughout the day among a diversity of shops, services and eateries. Transplanting the functional chaos of a mature streetscape to a new community remains an abiding challenge for planners.

In 2020, the City of Toronto released a 56-page document outlining all the elements of built-form it believed contributed to ground-level retail streetscapes. Tellingly, many of the images it uses to illustrate good retail come from two-storey high streets such as Queen Street East and Greektown on the Danforth. The document offers advice on where to place signage and how to situate utilities and supporting columns for retail that sits at street level below a high-rise building, it does little to address the trickiest part of the equation: how to fill those spaces with retail that works.

As the city’s guidelines assert, build it right and, “the quality and diversity of retail tenants in the area will improve. Residents will have local and convenient access to goods, services and job opportunities. Lively active streetscapes will be created that invite people to gather in the public realm and make walking a more enjoyable experience.”

Toronto’s history of condo retail tends to be dominated either by risk-tolerant expansionist chains (everything from Shopper’s Drug Mart to the Liquor Control Board of Ontario), or services like dentistry and dry cleaning. Frankly, these kinds of retailers could be found in any place, but Mr. Chan is hoping to build a destination-worthy streetscape that is it’s own specific place.

As a society we’ve become used to the idea that on some big purchases you can try before you buy: we test drive cars, we have open houses, there’s even free samples at the supermarket. As Mr. Chan notes, this is less common in the world of commercial leasing where a typical retailer might have to sign on for a five- or 10-year term. Pop-ups have become a way-station for retailers stuck between the decision to stick with what they have or to make a new a long-term commitment.

Concord’s pop-up destinations have also formed part of the tours and open houses for residential real estate brokers who are weighing dozens of preconstruction GTA condominium sites for clients, and sometimes themselves.

“One realtor was like, ‘Oh wow, there’s a new concept: I like that and I’m gonna talk to some of my clients,’ ” Mr. Chan said.

In the next few weeks Concord’s pop-up will be hosting a pet-friendly Santa Claus installation for condo dwellers looking for holiday pictures with the jolly fat man (the nearby mall Santas restrict pet pictures to an hour a day, apparently). It’s all part of the mix of turning a condo complex from a place to stay into a place to live.

Source The Globe And Mail. Click here to read a full story

Real Estate Investors Push For Improved ESG Measures In Commercial Property

Canada’s commercial real estate sector is striving to meet increasingly demanding environmental, social and governance standards, but the ESG is still greener on the other side of the world.

For example, experts say Canada is playing catch-up in the use of “green leases” – commercial tenancy agreements in which the landlord and the renter incorporate sustainability, socially responsible management and good governance into their property deals.

According to Tonya Lagrasta, head of ESG for Colliers Real Estate Management Services, in Toronto, “Canada is behind places such as the European Union. Many Canadian developers are moving ahead anyway – we’re seeing a shift – but the rules and regulations aren’t necessarily in place.”

“In North America we’re seeing more of a push toward stronger ESG standards coming from investors, while in Europe it comes more from regulation,” says Avis Devine, associate professor of real estate finance and sustainability at York University’s Schulich School of Business, in Toronto.

A study last year by Deloitte, Green Leases – in the ESG Context

, found that the European Union Commission gave green leases and other ESG measures in the property sector a boost in December, 2019, when it adopted rules specifying what makes these measures green.

“In North America we’re seeing more of a push toward stronger ESG standards coming from investors, while in Europe it comes more from regulation.

— Avis Devine, associate professor, Schulich School of Business, York University

Lenders, developers and tenants can consider deals to be green if they include goals for climate change, protecting and conserving water and biodiversity (on the property), controlling and minimizing pollution and moving toward a circular economy that recycles and reuses materials.

According to the Deloitte report, research by Savills Investment Management found that 73 per cent of the world’s institutional investors expect green lease clauses to be incorporated universally between tenants and real estate investment managers by 2029.

In Canada, the experts say that major commercial developers, such as Oxford Properties, BentallGreenOak and Brookfield Asset Management, are typically ESG leaders. “These tend to be companies that have global assets, including those in places where the ESG rules are more developed than in Canada,” Ms. Lagrasta says.

Developers and institutional lenders in Canada were getting more serious about higher ESG standards before 2019, “but the pandemic set things back,” says Ryan Riordan, finance professor at Queen’s University’s Institute for Sustainable Finance, Smith School of Business, in Kingston.

On the other hand, COVID-19 gave real estate developers the opportunity to look more closely at environmental issues such as indoor air quality, Dr. Devine says.

There’s more interest than ever in commercial property ESG measures, but the challenge now is to make physical changes to buildings, Dr. Riordan says.

“We’re making strides on the construction side of ESG, but it takes a lot of time to retrofit and replace buildings with ones of higher standards,” he says.

Retrofitting is a daunting challenge but one that experts consider necessary because buildings contribute nearly 40 per cent of the world’s carbon emissions that are linked to the global climate emergency.

Canada and other countries are struggling to achieve net-zero emissions by mid-century amid concern that if we don’t succeed, damage to the Earth will be beyond repair.

“We need to retrofit nearly all the standing dwellings in Canada, but we’re doing this at 1 per cent of them per year. If we don’t go faster, it will take about 70 years – we should be going three times as fast every year,” Dr. Devine says.

There’s also a strong business case for retrofitting old office buildings to make them more eco-friendly, Dr. Devine adds. It’s partly good marketing – white-collar employees are still only trickling back to offices in major Canadian cities, and when they do, they want to go back to good quality workplaces, she says.

“There’s a premium earned by environmentally certified buildings,” she explains. It shows up in better occupancy rates, more likely lease renewal and lower costs to finish off rehab work for tenants once the basic environmental work is done, she says.

“And after we account for higher rents or lower water costs, is there a market premium for being a leader in sustainability? Evidence says yes,” Dr. Devine adds.

A study by Smith’s Institute for Sustainable Financing, released in April, shows investing in carbon reduction “more than pays for itself in terms of avoided physical damage alone.”

The Physical Costs of Climate Change: A Canadian Perspective suggests the savings come even before “taking into account the potential economic benefits of transitioning to a low-carbon economy” for Canada’s entire GDP.

But green leases are only a small part of how commercial real estate developers are boosting their ESG credentials, Ms. Lagrasta says. “There’s more attention being paid now to the S [social benefit] and the G [governance],” she says.

Institutional investors are looking more holistically these days at potential risks, for example, the cost of urban sprawl and the potential financial benefits of diversity on corporate boards.

“There is deep corporate finance literature showing that we end up with better risk-balanced outcomes in our real estate [investments] if the management isn’t all male,” Dr. Devine explains.

Source The Globe And Mail. Click here to read a full story

Long-Term Office Outlook Appears Positive, Says Insider

As Dorothy wistfully states in The Wizard of Oz, “There’s no place like home.” But what are owners, investors and tenants in commercial real estate (CRE) to make of ongoing visions of tumbleweeds blowing through our downtown cores in the fallout of an unprecedented shift to working from home?

According to a recent report commissioned by the National Association of Industrial and Office Properties (NAIOP), Canada’s leading organization for CRE developers, owners and investors, the reality is far from dire. In fact, even if the road ahead still looks a bit rough, there are numerous indicators that, well within the next decade, that yellow brick road might just be paved with gold.

Positive economic impact

Prepared for the NAIOP by Toronto-based real estate services company Altus Group, Economic Impacts of Commercial Real Estate in Canada (2022 Edition) emphasizes Canadian CRE’s positive economic impacts in 2021: the generation of $148.4-billion in net contribution to the GDP; $67.5-billion in labour income for workers; and the creation/support of one million jobs (372,710 direct).

An attractive angle, even though office-space surpluses continue to be exacerbated by the pandemic, the work-from-home trend and the green-lighting of construction for new “trophy” locations. Retail also faces great challenges as the pivot to online shopping remains strong, whereas industrial is hot but faces demand-over-availability issues.

Still, Canadian CRE’s largest hurdle is those empty offices – a short-term problem expected to be much improved within a few years, according to Peter Norman, Altus Group’s vice-president and chief economist. Pandemic-related decline in employee occupancy notwithstanding – compared to prepandemic numbers, weekly in-office attendance is currently down to between 25 and 35 per cent, though numbers on weekend-adjacent days (Monday, Friday) fall lower – Mr. Norman says “the economy is growing, and the number of office workers is growing. We are going to grow ourselves out of the issue of surplus office space.”

“The office sector will continue to transition over the next few years and 2023 will see more of what we’ve seen this year – which is that as lease rollovers come up, lots of tenants are negotiating smaller spaces but often in better buildings. The flight to quality will continue.”

— Peter Norman, vice-president and chief economist at Altus Group

When this will happen is harder to pin down. To start with, office-lease terms typically run between five and 10 years whereas the slow restart from the pandemic’s sudden stop has barely been in effect for one year – which means that the majority of leases are currently in effect but by no means guaranteed to be renewed. Exacerbating this uncertainty is the age-old truism “location, location, location”: Buildings more than a half-century old no longer cut it as tenants require modern spaces of reasonable sizes.

Flight to quality

“The office sector will continue to transition over the next few years,” says Mr. Norman. “2023 will see more of what we’ve seen this year – which is that as lease rollovers come up, lots of tenants are negotiating smaller spaces but often in better buildings. The flight to quality will continue.”

It’s ultimately a problem of linear programming, which many lease-bound bigger businesses will simply ride out; growth economics dictate that a 200-person capacity space half empty today might be full, or even too small, in less than a decade.

The needs of smaller businesses are another matter, and greater fuelers of the flight. Matthew Kingston, executive vice-president of development and construction at H&R REIT, Canada’s third-largest real estate investment trust, cites further complications for the future of older CRE spaces, particularly in Toronto, where renovations and rebuilds alike are required to conserve a minimum of 100 per cent of current office space.

H&R REIT is currently requesting permission from the City of Toronto to preserve a downtown heritage building, 69 Yonge St., by converting it from 100-per-cent office to 100-per-cent residential. “It’s too small a floorplate – one-quarter the size of what an office user would want in today’s market,” says Mr. Kingston, who puts the building’s current vacancy at around 20 per cent and calculates a whopping 87 per cent vacancy within two years.

A lack of modernity is what’s making it hard to hold on to 69 Yonge’s tenants, not just limited to issues of spatial design but also infrastructure, in terms of telecom, ESG (environmental, social and governance investing) and more. Plus, given the building’s floor plate, these tenants’ smaller businesses are most likely to adapt by simply leaving.

“For them, erasing office rent from the overhead is a massive deal,” says Mr. Kingston. “When you have a team of five, seven, 20 people, it’s much easier than a company with thousands to suddenly say, ‘We’re going to pursue a work-from-home policy.’

”The City of Toronto is in the dark ages from the conversion standpoint,” says Mr. Norman of the one-to-one office space retention requirement, citing other Canadian centres that are incentivizing change, notably Calgary with an available collective grant fund of over $20-million.

Commercial real estate remains crucial to the Canadian economy, especially because the owners of Canada’s estimated 750 million square feet of office space are, for the most part, pension funds. “What happens to commercial real estate values is very important because of pension funds alone,” Mr. Norman says.

In the near term, outmoded office CRE will remain a major issue for employers and employees alike, but says Mr. Norman, “office isn’t dead – it’s just transforming really quickly and almost everybody is altering their premises to be more amenable to the new way of working,”

”There is uncertainty for up to the next 10 years but in the end, we are probably going to need a lot of the space that we already have – and we might eventually need more,” he adds. “Many businesses will just ride out that linear programming problem. If growth isn’t quite as fast as perceived adjustment, some might opt for space reduction.”

Positive change is predicted in the next few years, though the trend might be hard to discern at first. “We see people returning to the office in 2023, but with a hybrid approach where they spend one to two days a week working from home,” says Mr. Kingston. “Businesses are looking for larger floor plates to accommodate more interaction and collaboration and offer amenities and outdoor space as incentives to entice people into the office – as well as top-of-the-line infrastructure to support increased digital usage, ESG targets and air-quality concerns.”

Prime locations that have these attributes will perform strongly, he says, but other buildings that cannot offer these demands will continue to struggle to maintain, as well as attract, office users.

”The vibrancy and economic activity that occur in a downtown core obviously have to do with the operation of CRE buildings – and the people that come to them and what they do at lunchtime, after work and all the rest of it,” says Mr. Norman. “It’s ultimately the difference between a live and a dead downtown.”

Source The Globe And Mail. Click here to read a full story

Industrious Plans Second Toronto Flex Workspace

Flexible workplace company Industrious is launching its second Canadian location in Toronto, this time in partnership with Dream Office Real Estate Investment Trust.

Industrious, a New York-headquartered office co-working company, will open Industrious Financial Core at 30 Adelaide St. E. in Toronto in March 2023. It will be located inside the 18-storey State Street Financial Centre in Toronto’s financial centre.

Industrious says it will feature 650 seats and span 53,622 square feet, according to a company release issued this morning.

One of the key attractions of the location, Industrious says, is its accessibility through walking, transit, bicycling or car.

The Industrious Financial Core facility will offer amenities including 24/7 security, underground parking, plus nearby restaurants and a coffee shop. Industrious also notes nearby conveniences like the downtown Toronto PATH indoor pedestrian network, food and entertainment options, hotels, gyms, shopping and cafes.

“This is our first dot on the map in Toronto and Canada, a market we’ve been excited to enter for years,” said Doug Feinberg, senior director of real estate at Industrious. “Toronto has historically been one of the lowest-vacancy and highest-performing office markets in all of North America.

“This adds a location in the Financial Core and Downtown East submarkets, with great walkable amenities and great access to Toronto’s PATH and subway system.

“It’s a good entry point to the market with room for us to add to our footprint as we build our network to support work-from-anywhere models.”

Industrious in Canada and worldwide

The partnership with Dream Office REIT (D-UN-T), a Toronto-based real estate investor with $17 billion in assets, marks the second Industrious location in Canada.

The first location is also in Toronto and opened its doors in September. It is hosted on the fifth and sixth floors at 33 Bloor St. E. in a 17-storey, 291,579-square-foot mixed-use building.

That building is owned by Epic Investment Services.

The location, formerly operated by WeWork, was converted into an Industrious flexible workplace featuring 450 seats. Like the Industrious Financial Core, Industrious highlighted its proximity to transit and amenities.

Industrious says its newest Toronto location is part of a strategy to expand its international presence of over 150 locations in over 65 cities.

It has also acquired flexible workspace providers The Great Room and Welkin & Meraki in Asia and Europe, respectively.

The company says it added over 350,000 square feet in Singapore, Hong Kong, Bangkok, Paris, Brussels and Eindhoven to its workplace portfolio through the acquisitions.

Industrious plans to “double its international presence by the end of the year and remains committed to growing domestically,” the firm states.

In an interview with RENX when it opened the Bloor Street East facility, Industrious director of real estate Sam Segal said the company is “actively looking at all major Canadian markets, including more sites in Toronto, for future locations.”

There was no specific timetable provided by Segal.

Source Real Estate News EXchange. Click here to read a full story

GALA Buys Bradford Ind. Land, Plans 1.4M Sq. Ft. Of Space

GALA Developments has closed on the acquisition of a strategically located 101-acre site in Bradford West Gwillimbury, north of Toronto, where it plans to develop approximately 1.4 million square feet of industrial space.

The property at 3664 8th Line was acquired for $37 million in mid-October from a private investor based in Quebec, GALA vice-president of real estate development Vito Valela told RENX. The developer had it under due diligence for four months before closing on the deal.

The site in growing Bradford West Gwillimbury, where GALA also has land as part of the multi-developer Bond Head low-rise housing community, will provide easy access to the Bradford Bypass via a ramp from Highway 400. That four-lane freeway, which is in the very early stages of construction, will connect Highway 400 to Highway 404.

“We knew it was coming and we were strategic in our selection,” said Valela of the bypass. “The opportunity arose and we seized it.”

The 16.2-kilometre Bradford Bypass has drawn criticism from environmental groups and some residents living near the corridor, raising concerns about potential damage to protected areas of the Greenbelt. However, the Ontario government wants to have it completed by the end of the decade.

GALA’s site will have coveted visibility from Hwy. 400 as well as frontage on 8th Line and 5th Side Road.

Site offers flexibility

“That gives us flexibility in our planning and phasing,” said Valela. “You can work the development as the need arises as we grow our tenant base.”

GALA is targeting large logistics users, warehousing providers and last-mile delivery companies as tenants for its business park. It will see what the market demands and will be able to deliver spaces ranging from 50,000 to 500,000 square feet.

GALA is designing its block and lot plan and hopes to have a pre-application consultation with municipal planning officials in December to receive feedback.

The goal is to have all approvals in place in the first quarter of 2024, have site servicing begin in the second quarter, and to start construction of the first building in the fourth quarter.

GALA ready to talk to potential tenants

GALA is already welcoming inquiries from members of the brokerage community on behalf of their clients and prospects regarding leasing.

“We’ve got patience to allow the market to take its course, but we believe that the long-term prospects are very good and we’re in it for the long haul,” said Valela.

With the downturn in the economy leading some property owners to potentially pull back on development plans, Valela believes new acquisition opportunities may arise. While GALA will keep its options open, it will take a cautious approach since it already has several properties in its industrial and residential development pipelines in and around the Greater Toronto Area.

“We have some industrial assets where we are fortunate to have excess land,” GALA president John Gagliano told RENX. “With the rise in the demand and need for warehousing, we are expanding some of our warehousing footprints on our existing boundary lines.”

GALA and TGA Group plan to start construction on the expansion of a 28,000-square-foot industrial building at 20 Royal Gate Blvd. in Vaughan next summer.

Other planned industrial expansions are: 250,000 square feet at 25 Clayson Rd. in Toronto; 70,000 square feet at 2645 Skymark Dr. in Mississauga; and 15,000 square feet at 18 Ingram Dr. in Toronto.

GALA’s multifamily developments

Gala also has several multiresidential projects in the works.

Danny Danforth — a 10-storey, 140-unit condominium with 4,400 square feet of street-level retail space at 2359 Danforth Ave., just east of Woodbine Avenue, in Toronto — will begin occupancy in late March or early April.

Other projects are in the approvals process, including a high-rise condo at 438 Avenue Rd. in Toronto and a mixed-use community with three condo towers at 189 Dundas St. W. in Mississauga. There are a number of longer term residential sites being assembled or that are already part of GALA’s portfolio and in the planning stages.

“We want to bring on more residential when the time is right,” said Valela.

GALA and TGA Group

North York, Ont.-headquartered GALA was launched by the Gagliano family-owned and operated TGA Group last year to oversee the development of the property portfolio the company has accumulated over the years. TGA provides leasing and construction services and owns, operates and manages approximately 1.2 million square feet of industrial space.

TGA’s Access Restoration Services arm is a disaster mitigation and property restoration company.

“We came from a very simple and humble beginning,” said Gagliano of the company created by his father Anthony in 1959. “Our approach to the market is to create great relationships and value, and that’s obviously been a family-driven component for many, many years.”

GALA has grown from a five-person operation to 10 since inception. Valela expects that number to double again a year from now as the company continues to grow and more developments are advanced.

“TGA and the Gagliano family have patient resources to see us through good times and more challenging times,” said Valela. “That makes it a little bit easier.”

Source Renx.ca. Click here to read a full story

Toronto Industrial Market Has Millions Of New Sq. Ft. On The Way

Industrial real estate transactions in the Greater Toronto Area (GTA) may have slowed in Q3 and developers and landlords may be becoming more cautious in response to current economic conditions, but the outlook remains positive for the approximately 840-million-square-foot and growing market during the next year.

Rents continued to rise, the vacancy rate was at a record low 0.9 per cent during the quarter and demand continues to outpace supply, so the pieces are in place for continued activity.

“The fundamentals are still strong,” JLL executive vice-president and managing director of GTA office and industrial Jonathan Peretz told RENX. “Overall, the industrial market is still historically very active and demand is still very strong. That gives me a sense of optimism for the development community.”

There were 17.77 million square feet of space under construction, with 6.4 million of the total expected to be completed by the end of the year, according to a new JLL report.

“The rates of new supply and delivery slowed down a bit this year, but that’s because there was just a big surge of construction after the construction stoppages over COVID,” Avison Young research manager for suburban markets Warren D’Souza told RENX.

Third-quarter construction starts included Pure Industrial’s sites at 10 and 20 Whybank Dr. in Brampton – at more than 600,000 square feet – and BentallGreenOak’s sites at 1352 and 1362 Tonolli Rd. in Mississauga combining for 516,375 square feet.

Third-quarter completed projects

The largest completion of the third quarter was a 445,100-square-foot distribution facility at 1655 Reading Ct. in Milton built by Orlando Corporation and fully leased by Rockwool.

That was followed by a 216,100-square-foot building for Canadian Appliance Source at 27 Director Ct. in Vaughan, and a 139,000-square-foot building at 675 Harwood Ave. N. in Ajax owned by Triovest that was 60 per cent leased.

Although the GTA saw 1.8 million square feet of deliveries during the third quarter, according to JLL, 79.9 per cent of that was pre-leased.

“Developers, regardless of the economic headwinds, are still not running for the hills,” Avison Young principal of industrial and capital markets real estate Ben Sykes told RENX.

“No one is in a rush to do a deal. Groups are still being very selective on covenant and use, and a lot of groups do not want to split larger tracts and space.”

New developments coming soon

Orlando has a new 569,083-square-foot cross-dock distribution centre at 1890 Reading Ct. in Milton that will be available for occupancy in March. Sykes said a number of groups are looking at that site.

Sykes said Panattoni will deliver a 485,485-square-foot, spec-built facility at 100 Ace Dr. in Brampton in Q1 2023 and noted there are indications a transaction could be in the offing with a multi-national manufacturer.

Menkes is nearing completion of a fully leased 377,254-square-foot warehouse at 8205 Parkhill Dr. in Milton.

Sykes said Crestpoint Real Estate Investments Ltd. and Alberta Investment Management Corporation are delivering a 630,000-square-foot, spec-built facility at 3160 Derry Rd. E. in Mississauga and are in active negotiations with a potential tenant.

Oxford Properties broke ground on its 180-acre, 3.3-million-square-foot master-planned James Snow Business Park greenfield development in Milton in the third quarter.

The first phase will comprise nearly 1.6 million square feet and include 400,000 square feet of solar panels as part of its sustainability commitment.

Canada Post will become the owner of the largest industrial building in Canada to meet standards for net-zero emissions. The 585,000-square-foot processing centre at 1395 Tapscott Rd. in Scarborough is expected to open in March.

Toromont Industries announced plans to build a 137,000-square-foot remanufacturing facility on 30 acres in Bradford West Gwillimbury.

Leasing demand remains strong

Nine leases of more than 100,000 square feet were signed during the third quarter, including:

• Samsung’s renewal of 435,000 square feet at 8041 Fifth Line in Halton Hills;

• Traffic Tech’s renewal of 249,500 square feet at 550 Matheson Blvd. E. in Mississauga;

• Shein’s new lease of 166,700 square feet at 10 Canfield Dr. in Markham;

• Ontario Power Generation’s renewal of 158,200 square feet at 2555 Forbes St. in Whitby;

• Portside Warehousing’s new lease of 141,399 square feet at 3430 Harvester Rd. in Burlington;

• and Probus Logistics’ new deal for 122,900 square feet at 53 Mobis Dr. in Markham.

While new lease deals of more than 50,000 square feet declined 53.3 per cent quarter-over-quarter, several large pending deals are still in the works.

“We’re still seeing incredibly strong pre-leasing demand,” said Peretz, “and a portion of the space that’s not currently leased is conditionally leased. So I think what you’re going to see is more announcements over the next couple of months going into Q1 where deals will get finalized.”

H&M has leased all of a new 716,838-square-foot building in the GTA East Industrial Park at Salem Road and Kerrison Drive in Ajax.

Pet Valu has leased a 670,485-square-foot cross-dock distribution centre in Orlando’s new BramEast Business Park at 10750 Hwy. 50 in Brampton. It’s scheduled for completion next year.

“We’re not seeing any meaningful givebacks or large spaces coming back to the market with the current tenant demand,” said Peretz.

The largest pre-leasing project to come to market in the third quarter is Pure Industrial’s 1.2-million-square-foot Lakeridge Logistics Centre at 537 Kingston Rd. E. in Ajax.

Billed as the largest spec-built industrial building in Canadian history, it’s expected to be completed by Q4 2024.

Avison Young is representing the property and Sykes said it’s receiving inquiries from various groups. He believes the entire building will be leased to one tenant.

Different users driving demand

A new report from Avison Young says leasing demand over the past five quarters for spaces of 10,000 square feet and greater has been dominated by logistics and distribution (37 per cent), retail/e-commerce (20 per cent), manufacturing (17 per cent) and consumer goods and services (12 per cent) tenants.

Most of the investor demand for spaces of 10,000 square feet and up during the same time frame was driven by private investors (35 per cent), followed by private equity (23 per cent) and institutional investors (19 per cent).

Twenty-eight per cent of the buildings under construction are design-build while 72 per cent are speculative developments, according to Avison Young.

Despite Avison Young’s report noting the GTA market has 67 million square feet under construction and pre-construction, new deliveries will continue to be in short supply.

“We’re operating in such an undersupplied market across the board and specifically on small- and mid-bay space,” said Sykes. “The inventory that’s been added is all formatted to the larger 100,000-square-foot-plus marketplace.”

While industrial rents have risen dramatically, Sykes said high development costs would mean smaller spaces would have to charge rents of up to $25 per square foot to be feasible — and the market for that price isn’t there yet.

A more strategic approach could be taken

A slowdown in speculative construction, particularly by merchant developers and for projects that don’t have permits in hand, may be the result of higher interest rates and economic uncertainty now and going forward.

“Developers understand their supply chain and they understand timing,” said Peretz. “Looking at the market, I think you’re going to see landlords and developers take everything under a strategic approach.”

Peretz said tenants are paying for occupancy certainty and asking landlords and developers to provide construction schedules to demonstrate they can deliver projects on time.

“It’s more of a partnership than ever before,” said Peretz.

“If anything, we’ll start to see a little bit of product come back or be delivered that doesn’t get absorbed,” Sykes said of what could happen if economic headwinds persist.

“But that’s not necessarily a bad thing and kind of takes the market back from an undersupplied landlord market to more of a balanced market.”

Source Renx.ca. Click here to read a full story

Suburban Toronto Records First Period Of Positive Net Absorption Since Pandemic

Commercial real estate firm CBRE says for the second quarter in a row, the country’s suburban office vacancy level was lower than the rate seen for downtown regions.

The firm says the national suburban office vacancy rate was 16 per cent in its most recent quarter, while national downtown office vacancy sat at 16.9 per cent.

During the second quarter of 2022, seven out of 10 Canadian markets recorded tightening suburban vacancy, most often in larger magnitudes than were seen downtown.

Positive shift does not necessarily herald a recovery

The suburban Greater Toronto Area office market recorded roughly 457,000 square feet of positive net absorption over the quarter, CBRE’s report stated. This marks the first instance since Q1 2020 that net absorption has been overall positive.

These encouraging results were primarily driven by the Markham North and Richmond Hill submarket in the east and the Airport Corporate Centre submarket in the west, where 123,000 and 185,000 square feet of positive net absorption were recorded, respectively.

As the flight-to-quality trend seen throughout various markets in previous quarters continues, 60.2 per cent of the overall net absorption in the market was also accounted for by class-A space.

While this quarter’s uptick in leasing activity is encouraging and might signal a start of recovery from the effects of the pandemic, current economic uncertainty and a looming recession are likely to deter occupiers’ confidence in the market for a little while longer.

Suburban construction activity

Development in the suburban office market is slowly gaining traction. The total space under construction in the market has more than doubled year-over-year, with 675,000 square feet currently in progress.

The east market leads construction activity, with an estimated 473,000 square feet of class-A office space in the pipeline.

Metrus, which is currently developing the largest of the four eastern sites, continues construction of The Crosstown Place at 844 Don Mills Rd.

The 265,000-square-foot office tower has approximately 55 per cent of its space still available, as anchor tenant Celestica pre-leased the top three floors.

Construction at 60 Mobile Drive continues as well, with 76 per cent of the 124,000-square-foot redevelopment pre-leased to anchor tenant OSSTF.

Veering to the north market, G Group Developments is constructing the third-largest office project across the suburban markets, having broken ground late last year.

The 10-story mixed-use office tower is located at 5250 Yonge St. and will add 119,000 square feet of office space to the market, plus another 80,000 square feet of retail below.

The west market is trailing slightly behind the north and east in terms of the size of projects under construction.

However, it is the only suburban market to see new supply this year and is still expected to receive an additional 83,000 square feet of new supply over the next two quarters.

Suburban office summary

Despite uncertainty about future office demand – combined with a near-term economic slowdown, rising financing and construction costs and labour shortages – no developments have paused construction and landlords remain committed and optimistic.

Source Renx.ca. Click here to read a full story

How Much Warehouse You Can Buy Today Vs. 2021: Sellers, Take Note

GUEST SUBMISSION: The year was 2022 and it had been a relatively steady 40 years of declining interest rates from the peaks of 1981 where the Bank of Canada rate reached a whopping 21.46 per cent.

Many (most) of the current workforce had only ever seen downward-trending interest rates, with the youngest generation of adults viewing rates at historical lows as the “norm”. However, the time came to pay the piper for years of unsustainably cheap money when the global economy careened into increasing and relentless inflationary levels.

This prompted fiscal measures (a.k.a. rate hikes) in an attempt to control the effects of years of unwavering fiscal stimulus and heedless spending.

While the transitions through business cycles can affect consumer confidence and create uncertainty in the financial markets, it’s important to realize we are still a long way from 20 per cent interest rates, and remain, at present, in historical low territory.

Having said this, it’s obvious that a 3.25 per cent increase in the BOC benchmark rate over just a six-month period will have some tangible consequences.

I am going to outline the facts behind affordability in the commercial real estate sphere compared to 12 months ago.

We’ll also examine how this is affecting our owner/user clients (who would occupy their own building) and our investor clients (who are looking for tenanted assets with a return on their money). Spoiler alert . . . property values are (gradually) eroding.

I like flow charts, so I’ve provided a simplistic analysis through flow to outline some of the big-picture elements affecting the commercial real estate market in Alberta and more broadly across borders.

The aforementioned factors are affecting both owner/user businesses as well as investors who have been extremely active in recent years through the acquisition and sale of commercial real estate assets across the province.

Each purchaser is analyzing the current market fundamentals uniquely to their goals of ownership.

I’ll outline below the effect current market conditions are having on each group.

Owner/user perspective

The year was 2021 and business had been good!

You (business owner) were willing and able to put down 20 per cent equity on the purchase of a commercial real estate asset for your operation.

You had been quoted a monthly payment of $40,000 for a $10 million facility but, for reasons out of your control, could not close on that specific property. Fast forward 12 months – what could you buy today for the same payment?

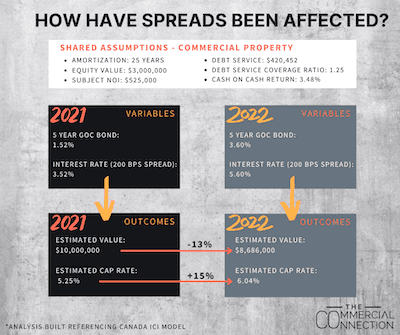

Generally speaking, spreads on five-year debt are about 200 bps over the five-year GOC Bond (up from 180 bps last year). This correlates to an estimated two per cent increase in interest rates in the past 12 months which seems minimal, but as you see from the image, can correlate to massive differences in affordability for a business owner.

Unfortunately, many industrial businesses in Alberta, particularly in the manufacturing sector, have been battling debilitating federal energy policies for the past seven years. This has prevented them from taking advantage of the low interest rates due to other market factors (even though most major markets in North America were on a 15-year tear).

While the above comparison is simple in nature, it highlights why so many deals have died over the past six months as purchasers on the cusp of affordability have had to transition back to the leasing market. It also highlights why there is heightened competition for smaller, lower-valued facilities.

Higher-priced buildings will be competing over a much smaller pool of qualified buyers as the interest rates continue to increase.

Investor perspective

Investors have been purchasing income-producing assets for record-setting low capitalization rates in recent years because the low debt costs allowed for return requirements to still be achieved.

It wasn’t uncommon for class-A multifamily assets to trade in the low four per cent cap rate range and commercial assets to trade low five per cent cap range, on average.

We’re currently sitting in a transition period where the mortgage interest rates have increased over two per cent in the past 12 months. However, seller cap rate expectations have lagged, overvaluing assets.

In fact, according to Brandon Kot, managing partner at Canada ICI: “If you indexed cap rates in Q3/Q4 2021 against interest rates during that period, values in multifamily assets would need to correct north of 20 per cent and commercial assets north of 15 per cent today in order to maintain the same levered returns. This doesn’t even take into consideration that yield expectations on the cost of equity have drastically changed in the last 12 months which would make a correction in asset values that much more acute. (The assumption on the level of value erosion is magnified in multifamily assets because of the prevalence of longer amortization periods (40 years plus).”

Looking at the following simple case study, I’ve compared an asset achieving an NOI of $525,000 in 2021 to today. In order for this asset to maintain the same DSCR and cash-on-cash return variables, the current value would reflect these downward pressures.

Ultimately, the market will dictate the price corrections that will take hold in the coming months, but it is important for building owners considering a sale of their properties to realize that these are the metrics purchasers are dealing with when determining today’s values.

The silver lining for some building owners is that if they have rollover or vacancy they may see improvements in their NOI due to increased market activity and competition for space. This improvement in rents and income could potentially increase in line with the upward adjustment of cap rates.

E.g. $525,000 NOI becomes $600,000 NOI on a 65,000-square-foot building. This $75,000 increase correlates to a $1.15-per-square-foot increase (from $8.08 to $9.23 per square foot), which is realistic in Alberta’s current industrial market. If cap rates were 5.25 per cent with $525,000 NOI, a $10-million valuation would be achieved. If cap rates increased to six per cent with $600,000 NOI, a $10-million valuation could still be achieved.

For those not experiencing these improvements in NOI, first, call an expert to assess the situation. Second, these assets do present a high probability of devaluation.

Source Renx.ca. Click here to read a full story

CanFirst Acquires $222.6M GTA Industrial Portfolio

The CanFirst Industrial Realty Fund VII LP has acquired a 13-property, 710,389-square-foot portfolio in Vaughan, Ont. from IG Investment Management for $222.6 million.

“We’re excited to be able to acquire assets in this node in Vaughan,” CanFirst Capital Management executive vice-president Mark Braun told RENX. “It’s always been a challenge to find properties in the area, certainly at a price point that’s competitive or allows us to transact.”

The portfolio encompasses 38.9 acres of land. The deal was brokered by CBRE and attracted interest from several potential purchasers.

The transaction, which closed Monday, represents a price of $313 per square foot.

All of the properties are located within about a kilometre of each other in Vaughan, and CanFirst is interested in acquiring more such locations in the city of approximately 340,000 people located directly north of Toronto.

Small and mid-bay properties

“It’s a mix of small-bay and mid-bay industrial tenancies,” said Braun of the portfolio.

The smaller units are in the 1,000- to 5,000-square-foot range while the largest is just over 50,000 square feet. The portfolio is 99.8 per cent leased, with just one small vacancy, and has an average remaining lease term of 2.5 years.

Braun said existing rents are about 50 per cent of the market rate, so the deal provides a good opportunity for capital growth when leases expire. There’s also potential to convert some units to industrial condominiums and sell them, Braun added.

The properties have been well-maintained and are in good condition and won’t require any major capital expenditures, according to Braun, who said there are no intensification opportunities within the portfolio.

CanFirst has been an active industrial buyer in recent months.

In October it partnered with Colonnade BridgePort to acquire a 50-acre site in the southwest sector of Ottawa. The partners plan to construct up to 900,000 square feet of new space on the land starting in 2024.

That site was acquired on behalf of its CanFirst Industrial Development Fund.

The last major acquisition for the Industrial Realty Fund VII took place in 2021, when it purchased the so-called Dozyn Dezyn portfolio, comprising 11 buildings in the communities of Surrey and Abbotsford, B.C. The small-bay and mid-bay buildings are a combined 412,897 square feet and were fully leased.

The purchase price was $104.5 million.

CanFirst Capital Management

Toronto-headquartered CanFirst was founded in 2002. It co-invests with institutional and private high-net-worth investors in industrial and office properties that have added potential to exploit for growth in major and select secondary Canadian markets.

CanFirst has raised $1 billion in equity and completed more than 16 million square feet of real estate transactions.

CanFirst manages growth-oriented and income-oriented funds. The $250.5-million CanFirst Industrial Realty Fund VII LP closed in July 2020 and is now fully allocated after this latest transaction.

Source Renx.ca. Click here to read a full story

44 Storeys Proposed Beside Eglinton GO Station

Like many of Toronto’s quieter neighbourhoods, Scarborugh’s Woburn is a lower density area amongst busier and and higher-density main streets. Now, MHBC Planning has submitted Official Plan Amendment and Zoning By-law Amendment applications that would result in the tallest building yet in this area, 44-storeys at 2941 Eglinton Avenue East, just east of McCowan Road at Eglinton GO Station. The proposal, designed by Kirkor Architects Planners for Achille Developments and 2941 Eglinton East Limited Partnership, would be in sharp contrast to the smaller buildings of the surrounding area.

The proposed design is 143.8m in height, with 555 residential units occupying the 44 floors of the structure. Residents would have access to 2,236m² of amenity space, of which 1,097m² would be outdoors. The gross floor area would total about 37,419m², with 288m² at grade being allocated to non-residential use. Below that, three levels of underground parking would house 278 spaces for vehicles and 416 for bicycles, of which 39 of the latter would be for short-term use.

There is currently a one-storey commercial building and parking lot on the site. The property is abutted by commercial and light industrial properties, some of it abandoned, with commercial strip buildings across Eglinton to the north. South of the GO corridor and north of Eglinton are neighbourhoods of apartment buildings, townhomes, and single-detached houses. Only a couple hundred yards from Eglinton GO station, the proposal is in a proposed Protected Major Transit Station Area (PMTSA), with the GO train allowing for access to Downtown Toronto and Durham Region.

The developer’s stated intent for the project is to complement the area and future potential developments. The building would feature step-backs throughout, with part of the goal being to act as a transition to the adjacent low-density area; this would include by the main entrances allowing pedestrians easy access to sidewalks.

Proposed landscaping incorporates planting beds and trees, with the intention being to create a comfortable public realm next to the building. Step-backs from the podium levels to the tower itself are designed to limit the impact of shadows on the immediate surroundings.

UrbanToronto will continue to follow progress on this development, but in the meantime, you can learn more about it from our Database file, linked below. If you’d like, you can join in on the conversation in the associated Project Forum thread or leave a comment in the space provided on this page.

Source Urban Toronto. Click here to read a full story

FOR LEASE – Retail Space – Toronto

Available area: 595 SF Lease rate: $1,800.00 Net Lease Located in Toronto’s upscale Leaside ne ...

BUSINESS FOR SALE – Sports Equipment Shop – Peterborough

Available area: 783 Sq Ft Asking Price: $300,000.00 An exclusive business opportunity awaits in Pete ...

FOR LEASE – Office Space – Toronto

Available area: 1,124 SF Lease rate: $17.00 Net Lease Perfectly located near the 401 with easy trans ...

FOR LEASE – Office Space – Toronto

Available area: 755 SF Lease rate: $1,800 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Scar ...

FOR LEASE – Office Space – Toronto

Available area: 638 SF Lease rate: $1,700 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Sc ...

FOR LEASE – Office Space – Toronto

Lease price: $23.50 Sq Ft Net + $17.68/2023/T.M.I. Available area: 3,901 Sq Ft 1,820 Sq Ft Elevate y ...

FOR SALE – Development Site – Woodstock

Size: 0.9 acres The two building lots are designed to be mixed-use, with commercial spaces on the gr ...

FOR SALE – Development Site – Woodstock

Size: 1.14 acres Currently has a commercial building whihc is built out for Resteraunt/Banquethall/ ...

![]()

Toronto Commercial Properties

Stephen & Mariya Lilly

Brokers

Office: 416-494-7653

Mariya Cell: 416-824-5078

Stephen Cell: 416-802-4228