Author The Lilly Commercial Team

Supreme Court Limits Governments’ Ability To “Constructively Take” Land

In a long-awaited decision, the Supreme Court of Canada has ruled on de facto expropriation of land.

In Annapolis Group Inc. v Halifax Regional Municipality, the Supreme Court provided guidance for situations in which the government essentially takes away land rights from property owners without formally expropriating the lands.

Although there is still a ways to go before the law in this area is settled, this decision is definitely a positive decision for developers’ and landowners’ rights in general.

Background and facts

Annapolis Group Inc. is a Halifax-based land developer which has been accumulating vacant land since the 1950s.

It had eventually amassed nearly 1,000 acres with the intention of developing it.

The Halifax Regional Municipality set out a new planning strategy in 2006 which identified part of the lands for possible use for a park in the future and denoted them as “Urban Settlement” and “Urban Reserve”, meaning the lands may be developed by the municipality within, or after a 25-year period.

Also, as part of the strategy, Annapolis was prohibited from developing the lands before the municipality adopted a “secondary planning process”.

Annapolis began seeking approvals to start developing the lands in 2007. In response, the municipality passed a resolution stating that it refused to initiate the secondary planning process “at that time”.

In the years that followed, the municipality encouraged the public to use the lands for outdoor activities such as hiking and camping.

Ten years later, Annapolis commenced legal proceedings against the municipality, seeking over $120 million in damages.

Annapolis alleged the municipality had effectively turned parts of the lands into a public park by encouraging members of the public to use them for outdoor purposes and therefore claimed damages based on de facto expropriation, unjust enrichment and abuse of/misfeasance in public office.

The municipality brought a summary judgment motion to dismiss Annapolis’ de facto expropriation claim, which was initially dismissed.

The Nova Scotia Court of Appeal later sided with the municipality and summarily dismissed Annapolis’ claim without allowing it to go to trial.

The court ruled the municipality did not commit de facto expropriation of the lands because no land was actually taken from Annapolis and the municipality therefore did not acquire a “beneficial interest” in the Lands.

It was also ruled that encouraging the public to use the lands and failing to adopt a development plan did not mean the lands were expropriated on a de facto basis.

The new test for “constructive taking” of land

The Supreme Court of Canada, however, saw things differently. The Supreme Court referred to de facto expropriation as “constructive taking”, as it applies to situations where a land owner alleges the state takes its land without formally expropriating it.

In other words, the state does not exercise its statutory authority to acquire an interest in the land and compensate the owner, but it does take steps to claim the land by other means.

In its decision, the Supreme Court held that, in order for “constructive taking” to occur, it is necessary to look at the intention of the government in exercising its regulatory authority and the owner’s loss of the use of the property. As such, the courts must look at what advantage the state obtained by the acquisition of the land and its effect on the property owner.

Therefore, in order for an “acquisition” by the government to occur, the property does not actually have to be acquired. If the government takes steps to acquire a beneficial interest in the property and the owner loses its reasonable use of the land as a result, the land can be deemed to be expropriated on a de facto basis (or “constructively taken”).

In applying the test in the Annapolis case, the Supreme Court held that there were more issues to unravel and therefore the Court of Appeal decision was overturned and the matter is to be determined by trial.

What this means

Although the law in this area is not yet settled, the Annapolis decision is being hailed as great news for developers and property rights holders in general.

It should be kept in mind the test for constructive taking is still onerous.

The court emphasized in this case that in order for it to occur, private property rights must be “virtually abolished”. And even where that is deemed to have occurred, it is not yet clear what it means for the government to gain a beneficial interest in the land.

In the Annapolis case, the court accepted that the government essentially using the land as a public park can constitute such an interest. Therefore if the public benefits from the land, that could be deemed to be a benefit to the state as well for the purposes of the test.

It will be interesting to see what will become of this decision going forward.

But for now developers should take note, as this case is definitely a step in the right direction.

To be clear, governments still have the power to expropriate land if the proper channels are followed. However, the Annapolis case shows courts may not have tolerance for the state using back-door means to deprive property owners of the benefits of their land.

Source Renx.ca. Click here to read a full story

How to Meet and Catalyze ESG Expectations in Canadian Real Estate

2023 promises to be another year with heightened focus on environmental, social and governance (ESG) compliance. The federal government’s 2050 pledge of achieving net zero status – either generating no greenhouse gas emissions or offsetting such emissions through tree planting or capturing carbon before it’s released into the air – is catalyzing the need for clean technologies and sustainable procurement.

With buildings, including homes, accounting for 12% of Canada’s GHG emissions, many property owners are utilizing ESG strategies to not only align with financial returns but with societal values as well. This behavioural shift will augment the value of ENERGY STAR® and GRESB certifications and industry standards for measuring and benchmarking energy performance across the country. For example, next year British Columbia will require ENERGY STAR certification for commercial buildings.

nvestment and community eyes on ESG

In this environment, tenants and real estate investors are casting an increasingly critical eye on ESG performance and risk. Ratings agencies such as Moody’s and S&P are also assessing corporations’ degree of ESG implementation more deeply. That means the focus on including investor relations because of the connection between ESG performance and capital markets.

“Buildings in several leading markets will need to achieve energy efficiency targets and greenhouse gas emission limits as early as 2024 or face significant fines. As investors increasingly demand newer, greener, and more energy-efficient buildings, particularly offices … older ‘brown’ buildings will see their values discounted, and their owners have trouble selling them,” says PwC and Urban Land Institute in their Emerging Trends in Real Estate 2023 report, which encompasses Canada and the U.S.

Leverage tech for compliance

With the ESG focus expanding beyond building operations to all aspects of portfolio management, many property owners are turning to advanced technology suites to monitor consumption and control costs. Implementation of a viable energy management strategy often begins with understanding and documenting energy consumption across a portfolio.

This is when software solutions that automate the management and analysis of utility expenses, utility bills and energy information deliver value. Property managers and operators can get valuable insight into energy consumption without having to dig through spreadsheets looking for outliers or missing bills.

Energy intelligence technology equally extends this capability, enabling building owners to identify incremental but powerful changes by comparing demand against consumption charges made by their utility providers. Another element of an effective energy strategy involves energy automation technology that detects faults and providing alerts on HVAC systems. Such systems can automate heating and cooling to optimize tenant comfort and minimize unnecessary costs.

The right energy management technology is built to help businesses deliver best-in-class performance.

Portfolio-wide visibility made easy

Energy management platforms are more than a dashboard or app. The solution you implement should seamlessly gather your whole building data and generate full visibility into energy consumption, from the building meter level, property-level analytics and benchmarking, all the way to owners, investors or lenders seeking insight into a portfolio’s energy risk. A site manager, for example, can compare a building’s energy performance against similar buildings in their region in real time, without having to wait for a certification process or energy audit.

The Yardi energy team has seen the benefits of advanced energy management software suites in property management organizations across Canada, including:

- 10-20% portfolio-wide savings, with low upfront costs and minimal tenant disruption.

- Higher property values arising from more efficient energy management

- A better occupant experience and higher retention with heating or cooling controlled with the minimum amount of energy required

- More effective property marketing with demonstrable operational improvements providing a competitive advantage

- Sustainability compliance that satisfies regulators, enables compliance with energy-use disclosure requirements and minimizes risk for potential investors.

As Emerging Trends in Real Estate 2023 notes, “At a time when financing is both less available and more expensive, companies with a strong ESG track record will have an advantage in attracting investment from institutional players and sourcing new forms of capital—such as green bonds and sustainability-linked loans—that continue to grow in Canada.”

Efficient energy management boosts business returns

Every participant in real estate management, from property managers to investors, seeks to reduce risk, increase efficiency, attract tenants and produce returns. A key element to achieving these outcomes is improving ESG performance. Just as a property management organization can’t operate with inadequate financial data, it can’t produce results with antiquated energy data or technology. Advanced energy management technology provides complete visibility and insight, drives informed decision-making, enables efficient portfolio management and adds value while reducing risk.

Source Real Estate News EXchange. Click here to read a full story

Nexus Buys, Sells, Builds as Industrial Transition Continues

Nexus Industrial REIT(NXR-UN-T) is continuing to buy and sell properties to reposition its portfolio and chief executive officer Kelly Hanczyk expects both transactions and development activity to remain brisk through 2023.

“We are continuing to grow an institutional-grade portfolio,” Hanczyk told RENX. “A lot of the products that we have coming on, and with the deals we have, are brand-new products.

“From a quality perspective, I think it will be second to none. Our fundamentals are strong. We have pretty good rental rate increases over the next year. I think everything looks stellar for a pretty solid 2023.”

Oakville-headquartered Nexus owns 113 properties, including two held for development in which the REIT has an 80 per cent interest, comprising approximately 11.1 million square feet of gross leasable area.

Nexus’ portfolio had an occupancy rate of 97 per cent at the end of September, consistent with the previous quarter and 200 basis points higher than Q3 2021.

Windsor and Tilbury acquisitions

Nexus most recently acquired a 435,871-square-foot portfolio of four industrial properties occupied by automotive component provider Plasman for $38.2 million on Nov. 1:

- 5250 Outer Dr., 5245 Burke St. and 418 Silver Creek Industrial Dr. in Windsor; and

- 24 Industrial Park Rd. in the small southwestern Ontario town of Tilbury.

“It was more opportunistic,” Hanczyk said of the acquisition. “We had an opportunity to buy them and the company’s got a pretty good covenant.

“The cap rate was really good and the price per square foot of the assets was really low. The in-place rents are well below market so, while it’s a long-term lease, there’s pretty good downside protection on it just from a market rent perspective.”

Nexus already owned two other properties in Windsor that are doing well and it plans to expand one of them by 65,000 square feet.

Other recent acquisitions

Nexus acquired a 38,400-square-foot industrial property at 605 Boundary Rd. in Cornwall, Ont. for $4.9 million on Sept. 30.

The building was occupied by Seaway Express, which was acquired by Canada Cartage in the fall.

“That was more of a relationship-driven deal,” said Hanczyk. “We wouldn’t usually buy a $5-million building, but it belonged to one of our existing tenants who we have a really strong relationship with and we want to be their landlord of choice.

“It was taking over a company and didn’t want to own the real estate, so we did a quick sale-leaseback with them.”

Hanczyk said Nexus will probably buy an industrial property being built for Canada Cartage in Calgary in 2024.

Nexus acquired a single-tenant 74,681-square-foot industrial property at 21800 Clark-Graham Ave. in the Montreal area for $17.8 million on Sept. 8.

It also acquired a single-tenant 94,000-square-foot industrial property at 50 Rue Lisbonne in the Quebec City area for $18.9 million on July 11.

“They were newer properties and solid assets with long-term, solid tenants,” said Hanczyk.

Development plans

Nexus acquired an 80 per cent interest in land located in Hamilton for $4.8 million on July 18. The REIT anticipates developing a 115,000-square-foot class-A industrial building on the site, with construction completion anticipated for early 2024.

The trust is in negotiations with an existing tenant for a 300,000-square-foot, build-to-suit industrial building on a property it already owns in Regina, where it has 23 acres of excess development land.

Hanczyk is hopeful ground can be broken on the project next spring.

“That would be a very attractive rate of return for us,” said Hanczyk.

Nexus is waiting on permits for a planned 100,000-square-foot addition to one of its properties in London, Ont. It was originally going to be built on spec, but the trust is in final negotiations with a tenant to lease it upon completion.

Hanczyk should know by January whether Nexus can move forward with a 65,000-square-foot expansion of a 130,500-square-foot facility it acquired last year at 70 Dennis Rd. in St. Thomas, Ont.

Selling properties and recycling funds

Nexus sold a retail property in Longueuil, Que. for $11.9 million on Oct. 4. It sold another retail property in Châteauguay, Que. for $8.3 million on Aug. 3.

The trust continues to soft-market several of its retail and office properties, sectors which now represent just 10 per cent of its total portfolio, and has an offer in play for another of its Quebec retail properties.

Nexus also received an unsolicited offer to purchase a small portfolio of industrial properties in Saskatchewan. That deal is now at the due diligence stage.

The REIT will continue to pursue capital recycling opportunities, with proceeds funding development projects expected to generate higher yields and to acquire class-A industrial properties in Ontario and Quebec.

“We are selling stuff, so that gives us free cash,” said Hanczyk. “We have an acquisition pipeline that’s fairly significant, so we’re able to transact if and when we want.

“It will just depend on how fast I can access or recycle that capital to allow me to buy additional product.”

Third-quarter results and stock performance

Nexus began to see the positive impact of rental rate growth in its industrial portfolio in Q3, with approximately 150,000 square feet of renewals and new leases commencing with rents at an average of $1.35 per square foot higher than expiring rents.

It has approximately 250,000 square feet of renewals and new leases starting this quarter with rents at an average of $2.50 per square foot higher than expiring rents.

Nexus had net operating income (NOI) of $24.87 million in Q3, which was $10.77 million higher than Q3 2021. Same-property NOI increased by about $300,000 during the same period.

The REIT had a debt-to-total-assets ratio of 47.2 per cent on Sept. 30. There was $60 million of availability on the REIT’s lines of credit and it had $59.4 million of unencumbered properties.

Nexus’ share price closed at $10.39 on the Toronto Stock Exchange on Nov. 18. That compares to a 52-week high of $14.03 and a 52-week low of $8.15. Its market cap was $608.02 million.

A joint venture between Singapore-headquartered investment firm GIC and Dream Industrial REIT announced on Nov. 7 an agreement to acquire Summit Industrial REITin an all-cash transaction valued at approximately $5.9 billion.

Hanczyk said Nexus’ share price is undervalued, but he believes it will rise and the trust will be the benefactor of exiting Summit unitholders looking to invest in another Canadian industrial REIT.

Source Real Estate News EXchange. Click here to read a full story

Debunking Commercial Real Estate Myths

Myths are described as either traditional stories of phenomenon, or more commonly, a widely held but false belief or idea.

I’ve tackled commercial real estate myths before but I think it’s due time to add a few more to the list.

Myth #7 – My buddy paid (insert silly value) right down the street for the same thing.

Not all commercial real estate sites are created equal.

Zoning can vary even on the same block as your buddy’s property. This will affect the allowable uses, which then affects the allowable tenants or buyers.

The more flexibility a site offers, the more attractive it can be.

Also, land relative to building structures plays a role in value. The percentage of land required versus the building is tied to use.

Land-shy properties become harder to accommodate business and therefore could be devalued.

There are many reasons why some sites might be worth more or less than their neighbours, so you can’t judge value by address alone.

Myth #8 – I’ve got plenty of time to get a lease in place.

Whatever time frame you’ve set aside for your search and lease negotiation, double it. Searching, viewing, securing and moving into a property can take a lot longer than you realize.

Decision-making timelines are well within your control, but be prepared to wait on the other side. Landlords are eager to lease vacancy, however they often have other businesses and believe it or not, they also have personal lives.

They can be unavailable to make snap decisions or be expedient in responding to offers.

The best way to bust this myth is to find out from the listing agent what kind of response time the landlord requires.

You may also need to engage third parties for part of the transaction and sometimes cannot speed up the wheels of bureaucracy.

Keeping on top of the professionals you’re using for reports or financing does often keep things rolling more smoothly than not.

Patience is a virtue, as they say.

Myth #9 – This building can be repurposed for the next person.

This myth comes with a caveat: while developers are mindful of building new structures that can be used for the most purposes, commercial assets can also have a shelf life.

It’s not uncommon that tenants, or owners, find themselves unable to utilize improvements made by previous tenants. So long as that can be torn out, though, the space can get a new lease on life.

Buildings that have been constructed with a specific use are the most obvious types in this category. A cost analysis could reveal that retrofitting a building might not be feasible.

The same can be said of older, functionally obsolete properties with dimensions that are simply no longer desirable to tenants.

Demolition and redevelopment of the site can be the logical step to recover the highest rents and most functional uses going forward.

Source Real Estate News EXchange. Click here to read a full story

STOREYS’ 2022 Commercial Real Estate Deal of the Year: Royal Bank Plaza Sells for $1.2B

With the real estate market moving from one extreme to another this year, those first couple of frenzied months — when people could actually afford to buy real estate, can you imagine?— are an increasingly distant memory. But as we close out the year, a transaction from back in January remains our pick of 2022’s most notable, earning it the title of STOREYS’ Commercial Real Estate Deal of the Year.

“These kinds of properties are an important part of our portfolio,” the statement goes on to say. The transaction is one of several big-ticket commercial purchases under Ortega’s belt, including two office buildings in Seattle, leased to Amazon and Facebook, a hotel in Chicago, and various properties in the UK. Ortega also owns office and retail real estate in Toronto’s Yorkville, so he is no stranger to the city’s real estate realities. “With the acquisition of Royal Bank Plaza, we increase our presence in Canada, one of the most stable countries and real estate markets in the world.”

Pontegadea also shares that there will be some improvements made to the building, including improving its energy efficiency and updating the interior spaces and common maintenance structures.

The sale of Royal Bank Plaza remains the largest Canadian commercial real estate deal — not to mention, among the biggest transactions for an office building globally — since the pandemic began. And as Keith Reading, Director of Research for Morguard, told STOREYS back in January, the purchase was a smart bet by Ortega on the resilience of Toronto’s post-pandemic office sector.

“It’s a world-class global market that’s still got one of the lowest vacancy rates in North America, and the building is fully leased with long-term leases, and one of Canada’s top banks is in there long-term,” said Reading, referring to the long-standing tenancy of Royal Bank of Canada. The company has around 40% of the building leased for the next decade. “It’s a good buy because these assets don’t come along very often; the buyer has secured control of one of Canada’s landmark buildings. It’s a world-class facility at centre ice in the downtown office market of a global city.”

TORONTO, CANADA – JULY 13, 2017: Golden Royal Bank Plaza skyscraper building facades in the Financial District of Downtown Toronto. View from below.

He added that while $1.2 billion is no chump change, Ortega snagged himself something of a once-in-a-blue-moon kind of deal — and rumour has it he was one of only two bidders.

“The price tag would have been north of $1.2 billion if there was no pandemic,” said Reading. “Prior to the pandemic, there was 2% vacancy in downtown Toronto, which put upward pressure on rent, so anybody who would have been looking to buy that asset would have looked at continued peak rent and room to grow, and the price would have been higher. Would it have been significantly higher? Not necessarily. It’s not a troubled asset; it’s a premium asset and this is a landmark acquisition. If people had the financial resources, and if there was no pandemic, you would have seen more bidders.”

Almost a full year after the sale, offices are welcoming employees back, downtown foot traffic has inched up, and the world has largely returned to its pre-pandemic ways, but the office real estate sector is yet to regain its pre-pandemic gusto. Still, Ortega’s investment shows resounding promise. This is something that Ray Wong, Vice President of Data Operations and Data Solutions at Altus Group, predicted with confidence in an interview from January.

“If you’re an employer, for your employees to get to an office across the street from the biggest transit hub in Canada is huge,” said Wong. “The sale is going to be a bellwether of confidence in the office market because it’s a fantastic downtown location and the acquisition price of $1.2 billion is pretty solid. They’re taking a long-term horizon on this asset.”

Wong continued, “It will take time for companies to come back, but there will be a little bit more demand for office space as people reconfigure their space needs and as other tenants begin looking for adjustments.”

In the meantime, the sector’s state of limbo certainly doesn’t take away from the notability of the Royal Bank Plaza deal itself. Pandemic pains aside, the changing of hands at such a monument was — and is — a huge moment in the world of Toronto real estate.

Reading said it best, “There are always new buildings in Toronto, but nobody is building another Royal Bank Plaza.”

Source Storeys. Click here to read a full story

Gen Zs Interested in the In-Office Experience, New Survey Finds

The return to in-person office work has been met with very mixed feelings. While some employers have pushed to get people back at their desks, many employees have pushed back. However, a new survey finds that Gen Zs are something of an outlier; they’re more interested in the in-office experience than their generational counterparts.

This is according to the 2022 Canadian Workplace Survey from the Gensler Research Institute, Gensler’s global research arm, which attributes the younger generation’s desire to be in the office to a “pent up demand for learning and career development opportunities.” The survey also finds that 43% of Gen Z respondents report coming into the office to access technology, 42% to attend meetings, and 39% to access specific spaces, materials, and resources.

Gensler’s research also explores why employees of other generations are motivated the return to the office, how the office can more effectively support them, and the strategic mix of design solutions and experiences that will accelerate their return.

Generally speaking, employees are open to returning to the office more frequently, “but only if the workplace offers the right experiences,” the research stipulates. “The quality of their office environments is holding them back.”

The survey finds that 24% of employees would be willing to return to the office full-time if provided a range of workspaces, while 42% would be willing to add an extra in-office day to their weeks. Diversifying the in-office experience stands to not only appease employees, but improve productivity at a time when the workplace’s effectiveness for focused work is at a 15-year low.

In addition, Gensler’s research shows that employees in high-performing workplaces are almost twice as likely to have a positive experience in the in-office format, citing benefits to personal well-being, career advancement, and job satisfaction. As such, those in high-performing workplaces express more willingness to return to in-person office work more regularly, suggesting that “the workplace can be a critical tool for talent attraction and retention.”

Source Storeys. Click here to read a full story

Blackstone To Buy Toronto Warehouse Portfolio For Over $400M

New-York-based Blackstone Real Estate has entered into an agreement to purchase six industrial properties in the Toronto area for more than $400M.

The properties’ locations have not yet been publicly disclosed, but are said total 1.5M sq. ft and are fully occupied, having traits seen as desirable to tenants such as being newer builds, having higher than average heights, and being in core infill locations.

“Global logistics is one of our highest conviction investment themes, and high-quality, last-mile industrial properties like these continue to benefit from some of the strongest real estate fundamentals in Canada,” Janice Lin, Blackstone’s Head of Canada Real Estate, said in a statement to STOREYS. “We look forward to continuing to grow our logistics portfolio, while supporting the supply chain in Toronto and providing best-in-class real estate to our tenants.”

The sale represents one of the largest private industrial portfolios to change hands in Canada since Blackstone’s 2018 privatization of Pure Industrial Real Estate Investment Trust — a transaction valued at $3.8B.

Although the seller has not yet been confirmed, a report from Bloomberg identified the the party as the asset-management arm of Toronto-Dominion Bank, according to an anonymous source. TD did not respond to a request for comment by the time of publication.

Even as Canada’s real estate market saw volatile fluctuations, the demand for industrial properties has remained strong, especially in the Greater Toronto Area. Last month, Thomas Cattana, Vice President at Colliers, said that Toronto-area vacancy rates are the lowest they’ve been in recent memory.

“If you look back 10 years ago, the availability rate would have been a number around 5%, and today that availability rate as of Q3 2022 is less than 1% — it’s 0.7%,” Cattana told STOREYS.

Source Storeys. Click here to read a full story

Adapt or Die: Why Converting Offices Into Homes Hasn’t Taken Off in Canada

Reduce. Reuse. Recycle. We all know these concepts as it relates to waste, but did you know they can be applied to buildings too? When it comes to real estate, they’re deeply-intertwined in what’s called “adaptive reuse.”

The concept is simple: take a building that’s run its course and convert it into something that suits the needs of the current time. Not only does this make use of a neglected or empty building, the companies that own and operate these buildings can also continue benefiting from their initial investments and save significant amounts of money they would otherwise need to spend on constructing an entirely new building.

One of the earliest examples of adaptive reuse also happens to be one of the most famous buildings in the world: The Louvre. Built in the late-12th to 13th Century under King Philip II, the Louvre was originally built as a defensive fortress for France. It was then converted into a residence in the 14th Century by King Charles V, and then became a residence for artists after King Louis XIV chose Versailles as his residence in 1682. The Louvre made its final transformation about a century later, opening in 1793 as the Musée du Louvre, now the most-visited museum in the world.

Over on our side of the pond, one of the first notable examples of adaptive reuse in North America was Ghirardelli Square in San Francisco. According to the Cultural Landscape Foundation, in the 1960s, architects Lawrence Halprin and William Wurster converted what was then a one-block plot with a chocolate factory into a shopping and tourist destination that’s still standing today, “creating a viable adaptive reuse model for other cities” in the process.

The trend didn’t exactly catch fire here in Canada, with the very-notable exception of the Distillery District in Toronto, which was originally established as the Gooderham and Worts Distillery. Distillery operations closed in 1990 and after gathering cobwebs for a while, re-opened to the public in 2003 as a commercial district that happens to include one of the largest collections of Victorian-era industrial architecture in North America.

Those three examples are all of conversions — sometimes also called “rehabilitations” — into commercial space, but nowadays what’s more common is turning commercial space into residential space.

Work From Home, Homes From Work

The world has just gone through a once-in-a-century event in the COVID-19 pandemic. Aside from changing how we think about things such as personal health, the pandemic also changed our relationship with space. Our homes used to be just that: our homes. These days, they’re increasingly doubling as places where we work, where we shop, and where we exercise. Because of this, spaces that once existed solely for those purposes are no longer as needed.

Many people purchased homes during the pandemic after realizing they needed more space to accommodate working from home. For a while, many office buildings, like streets and malls, became empty. Quite a few still are. Many people, now used to the benefits of working where they sleep, are not thrilled about returning to offices, and there aren’t strong indications that’s going to drastically change soon. Where does that leave office buildings?

You can’t exactly pick up an office building and drag it over to the recycle bin, but what cities around the world are now seeing is office buildings being turned into housing, particularly in places in dire need of it. Chicago is converting office buildings in its famous business district into apartments. New York City has created an Office Adaptive Reuse Task Force. California has passed legislation to encourage adaptive reuse, citing the state’s housing crisis. All of this happened just in the past few months.

According to the American-based National Apartment Association, 32,000 apartments have been created since 2020 as a result of conversions, including a record-high 20,100 in 2021, which included conversions of 7,400 offices, 3,400 factories, 2,850 hotels, and others. In March 2022, the NAA said they were expecting 53,000 more units in 2022.

Why are we talking about the US? Because here in Canada, we couldn’t be farther away from those numbers.

But Canada does have some examples.

In September, a redevelopment proposal was brought to the City of Toronto that would see a century-old office building restored and converted into a residential building. A similar planwas proposed for a different heritage office building in Toronto last December. On the West Coast, a 21-storey heritage office building in Vancouver was converted into a residential building called The Electra in 1995 that’s still going strong as a rental building. The historic Gastown area also continues to be restored, often with new uses.

Over in Calgary, 200,000 sq. ft of office space in the Palliser One building is set to be converted into 176 apartments, and if any city in Canada is leading the way on adaptive reuse, it’s the Stampede City. The City of Calgary has, by far, the most successful programs in the country — officially called the Downtown Calgary Development Incentive Program — that provide financial incentives specifically for conversions of office buildings into residential uses.

Calgary’s program wasn’t primarily birthed because the region desperately needed housing, or because they wanted to preserve heritage buildings, like the incentive programs in Victoria, Winnipeg, and Halifax. It was because they had an overstock of office space.

According to an economic report published by the City in November 2022, Calgary accumulated over 4M sq. ft of office space between 2013 and 2018. That was followed by a steep reduction in demand, by over 6M sq. ft, leaving Calgary with a bunch of office space occupied by nothing except dust. Since then, the City’s program has resulted in about 665,000 sq. ft of office space converted into over 700 homes, with more coming in Phase Two of the program.

But these are the exceptions in Canada. There has been little to no increase in adaptive reuse projects in Canada, let alone has the idea reached a critical mass, or a “tipping point” where the idea takes on a life of its own. Unlike in the States, statistics about adaptive reuse do not even exist and cannot even be compiled.

STOREYS reached out to Altus Group, a Toronto-based company that specializes in commercial real estate analytics, and a spokesperson said that they did not have such data. CBRE Canada and Avison Young, who regularly publish data reports about commercial real estate, were also reached and similarly did not have such data.

STOREYS also reached out to the Canadian Mortgage and Housing Corporation (CMHC), whose Rapid Housing Initiative specifically includes conversion projects. The CMHC has data about how much total units of housing have been created in Canada through the Initiative, but was unable to compile data specifically about units created via adaptive reuse, pointing only to examples of individual conversion projects that were previously announced. They estimated the grand total of housing units created via those projects to be at about 2,000.

The lack of such data is indicative of where adaptive reuse stands in Canada. On Everett Rogers’ famous Diffusion of Innovation curve, the concept of adaptive reuse in Canada is stuck in the Chasm. To identify why, it helps to understand the processes behind adaptive reuse projects.

How to Recycle an Office Building

Converting an existing office building into a residential building sounds cool, but it isn’t as simple as swapping out the furniture — like converting a spare bedroom in your house into an office. Buildings, regardless of how plain or basic they may appear, are designed for their specific intended uses. After all, before it began being used in other realms, “form follows function” was a maxim coined by an architect.

Because an industrial building can be drastically different from an office building, and an office building can be surprisingly different from a residential building, the building that’s targeted for conversion has to first be analyzed from top to bottom to see how feasible conversion really is, taking into account factors such as the structure of the building, its engineering, and even its aesthetics.

“These conversions are so asset specific,” Jessica Morin, Head of Research for CBRE US, told STOREYS. “The factors really have to be perfect: building, location, lighting, floorplates, attractiveness of the construction market, how quickly they can flip and lease it.”

Office buildings typically have larger floor-plates, because spreading out employees across multiple floors is more of a hassle than having them all on a single floor. Single-floor offices with open floorplans also facilitate communication, comradery, and cohesion (back before Slack was a thing). Offices also typically have washrooms clustered together, which means the plumbing of the building is quite different than in an residential building, where each unit in every corner of the floor has at least one washroom.

“Often, particularly in smaller or more rural municipalities, buildings are too old or too structurally precarious to support the business-case for adaptive reuse,” Alberto de Salvatierra, a professor at the University of Calgary’s School of Architecture, Planning, and Landscape — as well as the Founder and Director of the Center for Civilization, a design-research think tank — tells STOREYS.

“In these cases, it would just be too expensive to renovate. Demolition and reconstruction become surprisingly cheap in comparison. In other instances, available stock is spatially inadequate: in larger cities, like Calgary, vacant office buildings can have floorplates that are too deep or irregular to support the business case of adaptive reuse, or in smaller cities, like Medicine Hat, buildings are too small. When the motivation is to create dense, mixed-use developments and affordable housing, certain buildings simply cannot deliver.”

“It can be cheaper to demolish and build anew, particularly in cities where the land on which buildings sit has become more valuable that the building itself,” Professor de Salvatierra adds. “In these instances, developers would rather build a newer, taller, and more luxurious tower from scratch rather than try to adapt existing stock. Often, the biggest obstacle to adaptive reuse is the business case.”

In other words: a confluence of factors have to come together in a single building for a conversion to be the best approach — physically and financially. The more walls that have to be added into a building, the more money it’s going to cost. The more the office building’s insides have to be gutted, the more money it’s going to cost. Like it or not, developing housing is a business, which means if it doesn’t make money, it doesn’t make sense.

Adaptive Reuse in Canada: The Chasm

Would more incentives help? Asked this question, Morin and her colleague Eric Stavriotis, Executive Vice President in Location Incentives, say that CBRE US has been tracking adaptive reuse since 2016 and they have not seen a correlation between adaptive reuse projects and incentives. They’ve also not seen a material increase of adaptive reuse in the States, but it has been steady in recent years, with anywhere between 70 to 100 adaptive reuse projects of various kinds a year.

Stavriotis says that the question of making better use of existing buildings is being asked at the city and state levels, and many are increasingly looking at incentives, but many of them are still in the early stages and it’s too soon to tell if the incentives will make an impact. But he also stresses that “if the asset is right for [conversion] and the value gets low enough, and they can set the right rent, there doesn’t have to be incentives for this to take place.”

“Conversions may end up being a small share of the pie,” Stavriotis says, pointing out that only about 2% of US office stock has been converted since 2016. “But this is the time to look at it.”

Back in Canada, Professor de Salvatierra says that “adaptive reuse has been a longstanding interest and priority” in academia. “It is widely known that buildings themselves are a significant source of global CO2 emissions, so adaptive reuse — rather than demolition and reconstruction — is a more sustainable and environmentally friendly approach to city building. However, the “popularity” of adaptive reuse by the profession, or its adoption by industry, is uneven across geographies. Cities have varied and distinct challenges, and not all of them see the value or urgency of adaptive reuse.”

Another factor is office vacancy. In CBRE Canada’s Q3 Office market report, the national average vacancy rate of office space in Canada was 16.9% in downtown cores, nearly half of that of Calgary (32.9%), which had the highest office vacancy rate in the country. In Toronto, the vacancy rate is at 11.9%. In Vancouver, the vacancy rate is at 7.1%. You can’t convert empty office buildings into apartments if you don’t have any empty office buildings to begin with.

Perhaps governments on all levels need to examine adaptive reuse more. Perhaps developers need even stronger incentives, to make those not-quite-feasible conversions more appealing. Perhaps companies can be incentivized to move more operations to remote work, freeing up office space to be converted into housing. Perhaps the housing crisis needs to get even worse for people to really look at adaptive reuse. Or, perhaps we need to get with the times, because as they say: adapt, or die.

Source Storeys. Click here to read a full story

CRE Sees Strong Growth in 2021, “Asymmetric Impacts” Across Asset Classes

Although commercial real estate in Canada is yet to rebound from the pandemic, the sector still spurred notable economic benefits over 2021. On the whole, commercial real estate contributed a net of $148.4B to Canada’s Gross Domestic Product (GDP), created and supported 1M jobs — 372,710 of which were long-term, salaried positions, otherwise known as “direct jobs” — and generated $67.5B in labour income for workers. However, of the various commercial asset classes, some had a stronger year than others.

This is according to a report by Altus Group and commissioned by NAIOP Research Foundation to examine the economic benefits of commercial construction across commercial real estate in 2021.

“The pandemic has had asymmetric impacts on the CRE sector. Various asset classes have seen changes in valuations, and some have been repurposed,” the report explains. “For example, the transition to work-from-home and the acceleration of online shopping trends has reduced the value of some classes of office buildings (especially older or “B” and “C” class) and some categories of retail space and raised the value of clean, strategically located industrial distribution centres. Some of these trends may decelerate or reverse over time.

“The total value of commercial real estate transactions increased substantially in 2021 from very poor conditions in 2020. Industrial real estate accounted for the largest share of the investment value of those transactions. Commercial brokerage fees rose modestly in 2021, reflecting the recovery in transactions. Property management, asset management and landlord operations combined represent the largest single component of economic activity within the CRE sector.”

Industrial Construction Continues Pattern of Positive Growth

Canada’s industrial construction sector has observed steady growth not only in 2021, but over the past five years, including over the pandemic. Investment into the sector exceeded $16B in 2021, with the lion’s share of investment, 61%, related to new construction and the remainder related to the renovation and retrofitting of existing buildings.

The report notes that this growth may actually accelerate in the years ahead.

“The demand for industrial space continues to rise, with vacancy rates in many important industrial markets across the country remaining low. Industrial investment in recent years has been fuelled by transformation among many significant industrial users, including the rise of cannabis cultivation since its legalization and more recently the retail sector’s embrace of e-commerce and home delivery, which has spurred demand for additional logistics and distribution centres.

Multi-family Construction on the Rise, on Par With Rental Demand

Institutional investor-grade multi-family construction investment in Canada saw significant growth in 2021, rising to $24.1B.

This is largely attributed to investors accessing CMHC affordable housing incentive financing programs such as the Rental Construction Financing Initiative. Such incentives have served to return financially feasible to the sector for investors by reducing equity requirements and enabling higher loan-to-costs or loan-to-value ratios at below-market interest rates. The report further explains that “this reduces the cost of investment relative to condominium apartment development, which benefits from presale deposits that lower the costs of capital.”

The report goes on to say that growth in the country’s multi-family sector is expected to continue in tandem with rental demand.

“…an acknowledged housing shortage in Canada and the emergence of ‘Gen-Z,’ a large cohort of young people emerging into their prime rental years, will continue to create opportunities for multifamily investors looking to bring new apartment buildings to market. Although the commercial real estate industry faces challenges from the pandemic and slowing economic growth, it promises to continue to be a major contributor to the Canadian economy in the years ahead.”

Office Construction is Down, but Leasing Remains Strong

Although Canada’s office sector declined over the past two years, 2021 still saw a significant construction investment of $12.8B. The bulk of that investment (63%) was put toward new builds, and the remainder (37%) was put towards retrofits/renovations, including upgrades to HVAC systems.

Although investments in the office sector have risen since 2018, the report forecasts that the growth will likely taper off in the next few years as “post-pandemic trends may decrease the need for new office space at the same time as many office users find that adapting their spaces to emerging new working realities requires capital investment.”

With that said, leasing in the sector reportedly remains strong. Of the 17.2M sq. ft under construction across the country, pre-lease agreements account for just under 65%.

“This strong pre-leasing performance, even considering potential uncertainty regarding the amount of space required over the next few years given ongoing pandemic effects, reflects the strong flight-to-quality trends seen in many markets in recent years.”

Retail/Hospitality Construction Continues to Soften

Since reaching a peak in 2019, construction investment in Canada’s hospitality sector has seen downward pressure, falling 16% to $11.8B in 2021. This is certainly not surprising. The sector — particularly brick-and-mortar retail, hotels, and restaurants — was disproportionately impacted by the pandemic and is yet to recover.

That said, the report notes a “pent-up demand for in-person shopping experiences,” realized in 2021.

“Many markets across Canada saw a robust return of traffic and spending at brick-and-mortar retail locations, especially regional malls, as pandemic restrictions eased. To the extent that there has been a permanent shift toward e-commerce as a percent of retail sales, retailers are transitioning brick-and-mortar locations to focus on providing consumers with lifestyle shopping experiences, signalling the adaptability of retail to emerging trends and consumer preferences.”

Of the total investments, 55% of the retail investments were into new construction — “a trend that had been rising and peaked in 2020 with a modest decline in 2021.” This is perhaps reflective of some semblance of positivity amongst investors in the sector.

Source Storeys. Click here to read a full story

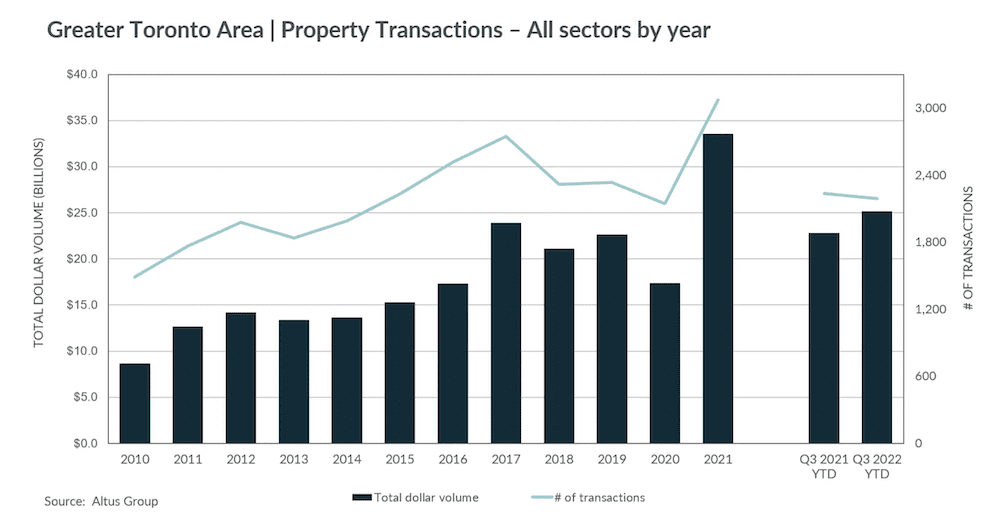

GTA Commercial Real Estate Investment Feels Rate Squeeze, Plunges 34% in Q3

It’s not just prospective homeowners feeling the pinch of rising interest rates — an overall higher cost of borrowing has had a heavy impact on the commercial real estate sector in the Greater Toronto Area, according to the latest third-quarter data from Altus Group.

The numbers show that, following a record-setting first half of the year, spending chilled considerably between July and September, with $6.1B in total investment outcome. That reflects a decline of 34%, with registered transactions down 24% compared to the same time frame in 2021.

From a year-to-date perspective, though, total investment volume comes to $25.1B, still up 10% on a year-over-year basis. However, as Altus writes in the report, “The buying frenzy witnessed in the first half has morphed into investors pausing and navigating cautiously amidst the continually rising interest rate environment.”

The Bank of Canada has raised interest rates a total of six times since March in order to combat soaring inflation. That has brought the benchmark cost of borrowing from a pandemic-era low of 0.25% to 3.75% today, a level not seen since April 2006. That has effectively thrown cold water on buying and investment intentions at all levels of the real estate market.

A rising cost of construction — exacerbated by inflation and borrowing costs — has also contributed to the commercial real estate sector’s decline. According to Altus, for the remainder of the year, it will be assets offering the greatest flexibility and redevelopment potential that will remain the most popular among investors, though the “cautiousness and uncertainty in investor sentiment will persist.” This will be especially apparent for those in the midst of obtaining financing for projects, as borrower criteria tightens up among lenders.

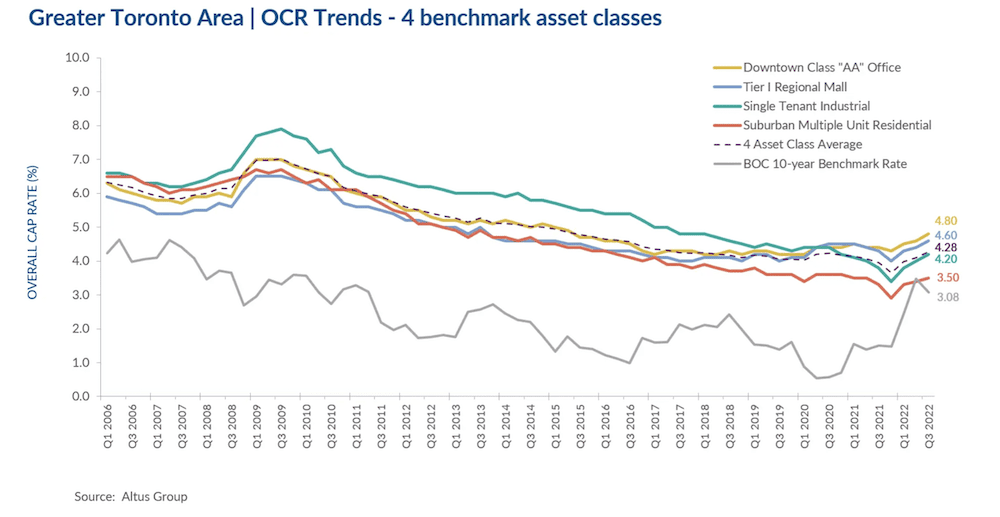

Due to this, Altus reports that cap rates have increased across all four major asset classes in the GTA: downtown class “AA” office, Tier 1 regional mall, single-tenant industrial, and suburban multi-unit industrial. An additional Investment Trends survey conducted by the advisory group revealed that, among participants, food-anchored retail strips, as well as suburban multi-unit assets remain the most coveted.

The office sector also remains a strong standout, with total investment doubling that of 2021 thus far at $3.5B. However, as Altus points out, this figure gets a notable boost by the sale of Royal Bank Plaza — which closed for $1.2B — in the first quarter of the year. The persistence of remote and hybrid work also continue to raise questions among investors about the viability of office demand into the near future.

Industrial space, meanwhile, continues to surge, given its steep scarcity of supply. Total industrial sales from the first three quarters of the year total $5.5B, just shy of the YTD $5.3B recorded in 2021.

“With GTA industrial vacancy rates continuing to hover around 1%, the demand for this asset persists,” writes Altus. “However, with an additional interest rate hike by the Bank of Canada anticipated in the fourth quarter, investors will continue to be cautious as the cost of capital increases.”

Overall demand for land in the GTA remained steady throughout the third quarter, with collective land sectors (residential lots, residential land and industrial commercial investment land) accounting for $11B to date – a 44% share of the pie for all commercial real estate deal volume this year. ICI land continues to be a strong presence, breaking the billion-dollar investment volume market for the sixth quarter in a row, while residential land showed signs of softening.

According to Altus, developers are indeed reducing their residential land acquisitions, or are pausing existing projects to ride out the rising cost of borrowing and labour. For the first time in four quarters, total investment for residential projects fell below the $2B-mark, with just $1.6B registered in Q3 — “a sign of caution after an enthusiastic previous four quarters.”

Source Storeys. Click here to read a full story

FOR LEASE – Retail Space – Toronto

Available area: 595 SF Lease rate: $1,800.00 Net Lease Located in Toronto’s upscale Leaside ne ...

BUSINESS FOR SALE – Sports Equipment Shop – Peterborough

Available area: 783 Sq Ft Asking Price: $300,000.00 An exclusive business opportunity awaits in Pete ...

FOR LEASE – Office Space – Toronto

Available area: 1,124 SF Lease rate: $17.00 Net Lease Perfectly located near the 401 with easy trans ...

FOR LEASE – Office Space – Toronto

Available area: 755 SF Lease rate: $1,800 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Scar ...

FOR LEASE – Office Space – Toronto

Available area: 638 SF Lease rate: $1,700 Gross Lease CLICK HERE TO DOWNLOAD THE BROCHURE Prime Sc ...

FOR LEASE – Office Space – Toronto

Lease price: $23.50 Sq Ft Net + $17.68/2023/T.M.I. Available area: 3,901 Sq Ft 1,820 Sq Ft Elevate y ...

FOR SALE – Development Site – Woodstock

Size: 0.9 acres The two building lots are designed to be mixed-use, with commercial spaces on the gr ...

FOR SALE – Development Site – Woodstock

Size: 1.14 acres Currently has a commercial building whihc is built out for Resteraunt/Banquethall/ ...

![]()

Toronto Commercial Properties

Stephen & Mariya Lilly

Brokers

Office: 416-494-7653

Mariya Cell: 416-824-5078

Stephen Cell: 416-802-4228